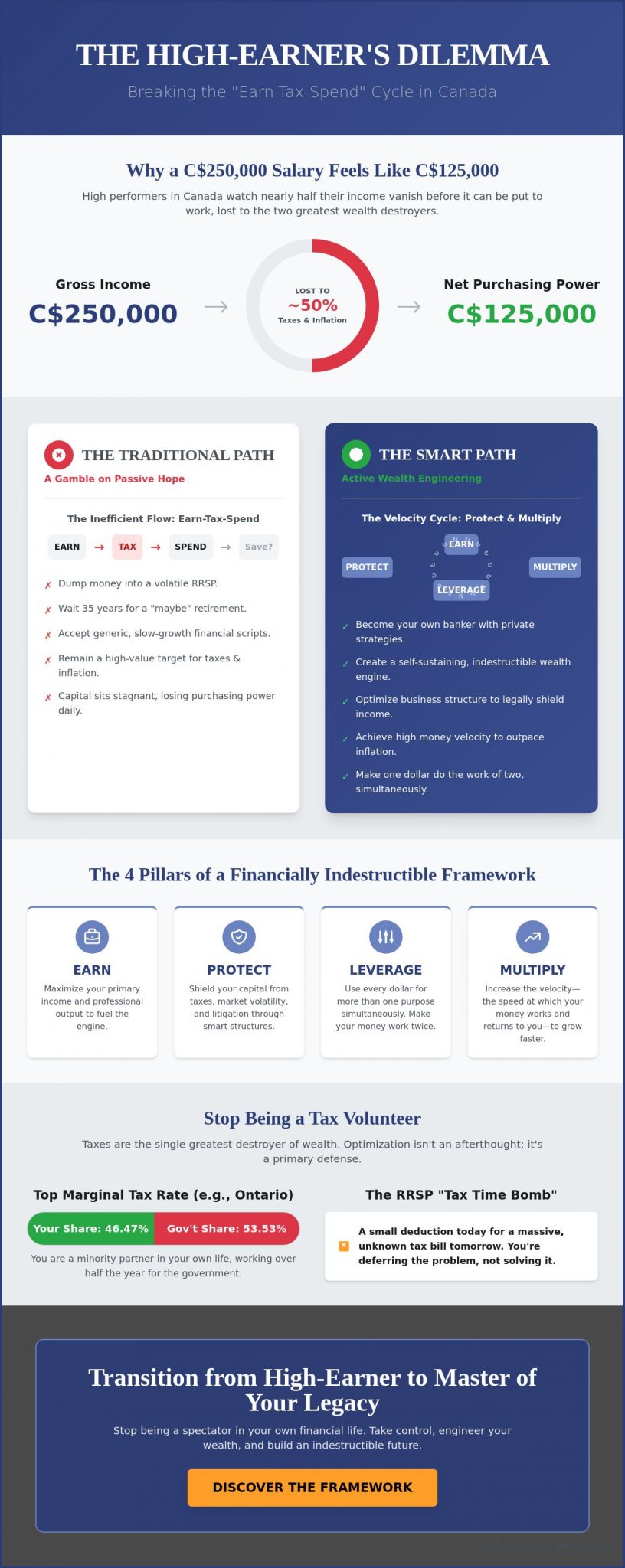

Stop measuring your success by your gross earnings. If you’re a high-performer in Canada, you already know that a C$250,000 salary often feels like C$125,000 after the CRA takes its cut and inflation erodes your purchasing power. Traditional advice tells you to dump money into a volatile RRSP and wait 35 years for a maybe. That’s not a strategy; it’s a gamble. True income made smart requires a radical shift from passive saving to active wealth engineering. You need a system that doesn’t just grow but protects your legacy from the ground up.

I know you’re tired of watching 50% of your hard work vanish into taxes while your financial advisor offers the same generic, slow-growth scripts. You’ve mastered your craft, now it’s time to master your capital. I promise to show you how to transform your earned income into a self-sustaining wealth engine using the Financially Indestructible framework. We are diving into the 2026 roadmap to becoming your own banker and securing a legacy that is truly indestructible.

Key Takeaways

- Break the cycle of “earn-tax-spend” by adopting a velocity-optimized model that protects and multiplies your wealth automatically.

- Stop being a tax volunteer to the CRA and discover how smart business optimization can legally shield your C$ from the single greatest destroyer of wealth.

- Turn your capital into a self-sustaining engine using private banking strategies that allow one dollar to do the work of two simultaneously.

- Discover why income made smart requires high money velocity to outpace inflation and eliminate the hidden opportunity costs of stagnant savings.

- Transition from a high-earner to a master of legacy by implementing a framework designed for total financial indestructibility in the Canadian market.

What Does ‘Income Made Smart’ Actually Mean in 2026?

Stop thinking about your paycheck. Start thinking about your flow. In 2026, income made smart isn’t a luxury; it’s your only defense against a volatile Canadian economy. Traditional income management is a relic. The old earn-tax-spend-save loop leaves you vulnerable to inflation rates that hit 40 year highs recently and tax brackets that punish your hard work. Smart income is different. It’s income that is protected from predators, leveraged for growth, and optimized for velocity.

You aren’t just looking for a steady stream of cash. You’re building a fortress. This means moving from a fragile state to being Financially Indestructible. This concept goes beyond the standard definition of financial independence. While independence means having enough to cover expenses, indestructibility means your wealth grows regardless of what the Bank of Canada does with interest rates. You must shift your model to a four pillar strategy:

- Earn: Maximize your primary output.

- Protect: Shield your capital from the CRA and market volatility.

- Leverage: Use every dollar for more than one purpose simultaneously.

- Multiply: Increase the speed at which your money returns to you.

The Myth of the High Salary

A high salary is a massive liability if you don’t have a strategic framework. If you’re a Canadian professional earning C$200,000 or more, you’re likely a Tax Volunteer. You’re handing over nearly half your output to the government because you lack the structure to keep it. High earners without protection are just high-value targets for inflation and litigation. The wealth gap is the direct result of stagnant capital sitting in accounts that lose purchasing power every single hour.

The Shift from Passive Saving to Active Mastery

Traditional advisors want you to set it and forget it. Why? Because they get paid while you sleep, even if your portfolio is bleeding out. That’s not a strategy; it’s a surrender. Taking the steering wheel of your private economy is the only way to win. You need income made smart to ensure every dollar works double duty. To build this foundational mindset and stop being a spectator in your own life, you need to grab Michael Santonato’s book immediately. Mastery requires action, not passive hope. Your legacy depends on your ability to pivot from a saver to a master of your own financial destiny.

Tax Efficiency: Stop Being a Tax Volunteer

You work hard for that C$50,000 bonus. You check your bank account and see C$26,000. It feels like a punch to the gut. Where did the rest go? It vanished into the void of the CRA. Taxes are the single greatest destroyer of long-term wealth for high earners in Canada. In provinces like Ontario, the top marginal tax rate hits 53.53 percent. That means you are a minority partner in your own life. You are working more than half the year just to fund the government’s budget. This is not just a financial issue; it is an emotional drain that kills motivation.

Stop being a tax volunteer. There is a massive difference between tax evasion and tax optimization. Evasion is illegal and leads to ruin. Optimization is the hallmark of a sophisticated professional. It is about using the existing rules to your advantage. True income made smart requires a shift in perspective. You must view tax-free wealth planning as a core pillar of your strategy, not an afterthought. Proactive Tax Efficiency is a year-round discipline that separates the wealthy from the merely well-paid.

Strategic Tax Optimization for Business Owners

Most accountants are historians. They look in the rearview mirror and tell you what you owed last year. That is a failure of leadership. As a business owner, you need a strategist who looks through the windshield. You can restructure your income to minimize the bite of national and regional authorities. By utilizing specialized corporate structures, such as Canadian Controlled Private Corporations (CCPCs), you can protect your annual earnings from unnecessary exposure. This is about mastery of your craft. Why let 50 percent of your profit leak out when you could reinvest that capital into your legacy? If your current advisor isn’t bringing you proactive ideas to cut your tax bill by 20 percent or more, they are costing you a fortune.

The RRSP Tax Time Bomb

The RRSP is often sold as the ultimate savings tool. It is actually a tax time bomb. You get a small deduction today, but you are deferring a massive, unknown tax debt to your future self. Who says tax rates will be lower in twenty years? With government spending hitting record highs in 2024, it is a massive gamble to assume rates won’t climb. Income made smart involves paying taxes now at a known rate to enjoy tax-free growth and withdrawals later. Transitioning from traditional, restrictive accounts to more flexible income vehicles allows you to maintain control. You deserve to know exactly what you keep. If you want to stop the bleeding and start building real momentum, it is time to audit your current tax strategy and find the hidden leaks.

Private Banking vs. Traditional Saving: A Smarter Comparison

Most Canadians are playing a losing game with their eyes wide open. You deposit C$10,000 into a “high-interest” savings account. The bank pays you a measly 1% or 2%. Then, they turn around and lend that same money back to your neighbors at 9% for a car loan or 19% on a credit card. Why are you subsidizing their record-breaking quarterly profits? Real income made smart starts when you stop being the bank’s most profitable customer and start becoming the banker yourself.

The Infinite Banking Concept (IBC) is the ultimate tool for financial indestructibility. It uses dividend-paying whole life insurance as a personal, private vault. Unlike a standard bank account where your money sits stagnant, this system provides uninterrupted compounding. Your capital grows every single day, regardless of market volatility or what the Bank of Canada decides to do with interest rates. You aren’t just saving; you’re building a fortress. Why would you let a bank profit from your money when you can capture that growth for your own family?

How the Infinite Banking System Works

The mechanics are simple, but the impact is massive. You don’t “spend” your savings anymore. Instead, you utilize the cash value of your policy as collateral. This allows you to fund your life’s major expenses while your original capital remains untouched and growing. Here is how the flow of a dollar looks in an IBC system:

- Step 1: You capitalize your system by paying premiums into a specially designed policy.

- Step 2: Your cash value builds tax-advantaged with guaranteed growth.

- Step 3: You need C$50,000 for a new equipment purchase or a business investment. You take a policy loan from the insurance company.

- Step 4: Your original C$50,000 stays in the policy, continuing to earn compound interest and dividends as if you never touched it.

You’re using the insurance company’s money to fund your lifestyle while your own money never stops working. This is the definition of efficiency. You can learn more about mastering these structures at True Financial Education.

The Efficiency of the Private Vault

Compare this to the restrictions of government-sponsored accounts. RRSPs lock your money away until you’re 71, and you’re taxed heavily on the way out. TFSAs have strict contribution ceilings that limit your growth potential. A private banking system offers total liquidity. It’s your money. You control it. You decide when and how to deploy it without asking for permission from a loan officer.

Don’t fall for the trap that life insurance is only for when you die. That’s old-school thinking for people who aren’t paying attention. This is a living asset. It’s about income made smart through every stage of your career. By reclaiming the interest you’d normally give to a third-party lender, you’re keeping the profit in your own pocket. That is the ultimate act of financial independence. It’s time to build a legacy that provides impact today and security tomorrow.

Engineering Velocity: Making Every Dollar Do Two Jobs

Money velocity is the heartbeat of your financial survival. It’s the speed at which a single Canadian dollar moves through your personal economy to acquire assets, pay expenses, and return to your pocket. Most people let their money sit. They park it in “high-interest” savings accounts earning a measly 1.5% while inflation in Canada averaged 3.9% in 2023. Stagnant money isn’t just resting; it’s dying. You’re losing purchasing power every second your capital isn’t in motion.

To achieve a state of being financially indestructible, you must stop viewing expenses as terminal points. Every C$1 that leaves your hand must be an employee sent out to bring back more friends. This is the core of income made smart. You aren’t just earning; you’re engineering a system where lifestyle purchases, like a new vehicle or a home renovation, simultaneously fund your estate. You don’t choose between spending and saving. You do both with the same dollar.

The indestructible mindset demands that every expense becomes an investment. If you’re paying for it, you should be profiting from the process of financing it. This isn’t a luxury for the ultra-wealthy. It’s a mandatory shift for anyone tired of the traditional Canadian banking trap that keeps your velocity at zero.

Debt Restructuring as a Wealth Tool

Stop fearing debt and start categorizing it. Consumer debt is a parasite that sucks your cash flow dry with 19% or 24% interest rates. Strategic leverage is a precision tool used to build empires. By using private banking structures, you can wipe out high-interest liabilities permanently. You become the source of your own financing. Strategic Recapture is the deliberate act of reclaiming interest volume that would otherwise flow to external financial institutions and redirecting it into your personal wealth cycle. This move alone can save the average Canadian family over C$100,000 in interest costs over a decade.

Private Money Maximization

When you master income made smart, you stop being a borrower and start acting as a private lender. You position your capital in assets that are shielded from creditors and tax-efficient under Canadian law. This isn’t just about growth; it’s about legacy. You’re building a fortress that keeps your family’s wealth inside the family. Many professionals lose up to 15% of their annual cash flow to “leaks” they can’t even see. Professional coaching identifies these hidden drains, ensuring your money velocity remains at peak performance. It’s time to stop the bleed and start the build.

Are you ready to stop losing money to the banks and start recapturing your wealth? Book your strategy session now to engineer your money velocity.

Mastering Your Legacy: The Path to Financial Indestructibility

Earning a high salary is a skill. Managing that wealth is a discipline. Mastering it? That is a legacy. You have spent your career trading time for Canadian dollars. Now, the shift must be absolute. To achieve true financial indestructibility, you must transition from a laborer of your own capital to an architect of an empire. This is income made smart in its purest form. It is not about chasing the next volatile trend. It is about building a fortress that stands regardless of what happens in Ottawa or on Bay Street. You don’t need more “tips.” You need a system that survives reality.

Most people drown in abstract theories. They listen to “experts” who have never managed a P&L or stared down a complex tax audit. You don’t need more ideas; you need a pragmatic roadmap. My Financially Indestructible Coaching Program exists because the traditional financial industry is broken. It’s designed to keep you liquid, tax-efficient, and in total control of your trajectory. We strip away the fluff and focus on the mechanics of high-performance wealth. Mastery is not a gift. It is a calculated decision you make today. Stop playing defense with your life.

The Wake Up Call: Why You Need a Strategy Now

Waiting for the “perfect moment” is a losing game. By 2026, the Canadian economic landscape will have shifted again. With debt-to-income ratios hitting record highs and tax regulations tightening, your old playbook is obsolete. You cannot afford to be reactive. You need to be bulletproof. If you are still operating on 2019 logic, you are already behind. The volatility of the current market makes these strategies essential, not optional. Start your transformation by enrolling in The Wake Up Call course. Stop guessing. Start executing.

Your Next Moves for Income Mastery

Action is the only thing that creates results. Stop overthinking and start auditing. Your path to income made smart begins with these three non-negotiables:

- Tax Audit: Stop overpaying the CRA. Identify every deduction and structural advantage available to your specific situation.

- Debt Evaluation: Not all debt is equal. Pivot from consumer liabilities to strategic leverage that builds equity.

- Liquidity Check: Ensure you have the cash flow to seize opportunities when the market dips. Cash is only king if you can access it.

Don’t leave your future to chance. Your legacy deserves a professional framework, not a series of lucky breaks. Mastery is a choice you make, or it is a regret you carry. Book your strategy session at True Financial Education right now. Let’s build a foundation that cannot be shaken.

Stop Playing Defense and Start Building Your Legacy

You’ve seen the blueprint for 2026. Financial survival isn’t enough; you need a strategy that turns every C$1 into a high-performance asset. Stop being a tax volunteer for the CRA. By leveraging the Infinite Banking Concept, you create the velocity needed to make your capital work twice as hard. This is the foundation of income made smart, a framework built on over 14 years of expert mentorship for North American professionals. It’s time to cut through the noise and focus on direct, results-oriented coaching that secures your family’s future.

Traditional saving is a slow leak in your financial boat. Real wealth requires mastery and a commitment to engineering your own private banking system. Don’t leave your legacy to chance or market volatility. You have the tools to be financially indestructible; now you just need the discipline to execute. It’s your move.

Your future is waiting for you to lead. Let’s build something that lasts.

Frequently Asked Questions

Is “Income Made Smart” just another name for tax avoidance?

Income made smart is about legal tax efficiency and wealth optimization within the framework of the Canadian Income Tax Act. You aren’t hiding assets or dodging responsibilities. Instead, you’re positioning your capital where the government provides incentives for growth and protection. This strategy helps you keep more of your C$200,000 plus income by using the same tools the wealthiest families have used for 100 years. Stop overpaying the CRA and start building your own legacy.

How does the Infinite Banking Concept apply to someone with a high salary?

High earners use Infinite Banking to stop leaking interest to commercial banks and recapture their purchasing power. If you earn C$250,000 annually, you’re likely paying significant interest on mortgages, vehicles, or business equipment. By becoming your own banker through a participating whole life policy, you recycle that capital. This creates a dual compounding effect where your money works in two places at once. You gain total control over your cash flow without begging a loan officer for permission.

Can I implement these strategies if I already have an RRSP?

You can absolutely integrate this strategy with your existing RRSP or TFSA. These accounts are useful tools, but they often lack the liquidity and control needed for true financial indestructibility. By 2026, the goal is to diversify your tax exposure. Use your RRSP for the immediate deduction, then use the smart income strategy to build a liquid, tax free pool of capital for immediate opportunities. Don’t lock all your money away until you’re 65; you need access now.

What is the “Financially Indestructible” framework?

The Financially Indestructible framework is a four pillar system designed to protect your wealth from market volatility and tax hikes. It focuses on liquidity, control, legacy, and guaranteed growth. Unlike traditional buy and hold strategies that saw the TSX drop 12 percent in 2022, this framework ensures your capital remains accessible. It’s about building a fortress around your family’s future. You stop playing defense and start playing offense with your money regardless of what the economy does.

How much time does it take to manage a private banking system?

Management takes less than 15 minutes per month once your system is established. Most of the heavy lifting happens during the initial design phase with your specialist. After that, it’s about automated deposits and periodic reviews to ensure your strategy aligns with your 10 year goals. You’re an executive, not a bookkeeper. Your time should be spent on high value activities that grow your business, not chasing paper or monitoring daily stock market fluctuations.

Is coaching necessary, or can I do this on my own?

You can read the books, but professional coaching provides the 100 percent accountability needed for true mastery. Most professionals fail because they lack the discipline to execute complex financial maneuvers when life gets busy. A coach identifies the blind spots in your cash flow that cost you thousands in lost opportunity every year. Do you want to guess with your family’s legacy, or do you want a proven roadmap to success? High performance requires a high level mentor.

What happens to my smart income strategy during an economic downturn?

Your income made smart strategy is built to thrive when the market bleeds. Because the core of the system relies on guaranteed annual dividends from mutual insurance companies, your principal remains safe from market crashes. During the 2008 financial crisis, while others lost 30 percent of their portfolios, these systems continued to grow. You gain the “opportunity fund” needed to buy assets when they go on sale. While everyone else panics, you’re looking for the next big win.

Does this strategy work for both Canadian and US residents?

This strategy works in both countries, though the specific tax codes and vehicles differ slightly. In Canada, we focus on the Income Tax Act and specific Canadian life insurance carriers. US residents use the Internal Revenue Code Section 7702. The mechanics of the Infinite Banking Concept remain the same across borders. Whether you’re in Toronto or Texas, the goal is the same: absolute control over your capital. We tailor the structure to your specific residency and tax obligations.