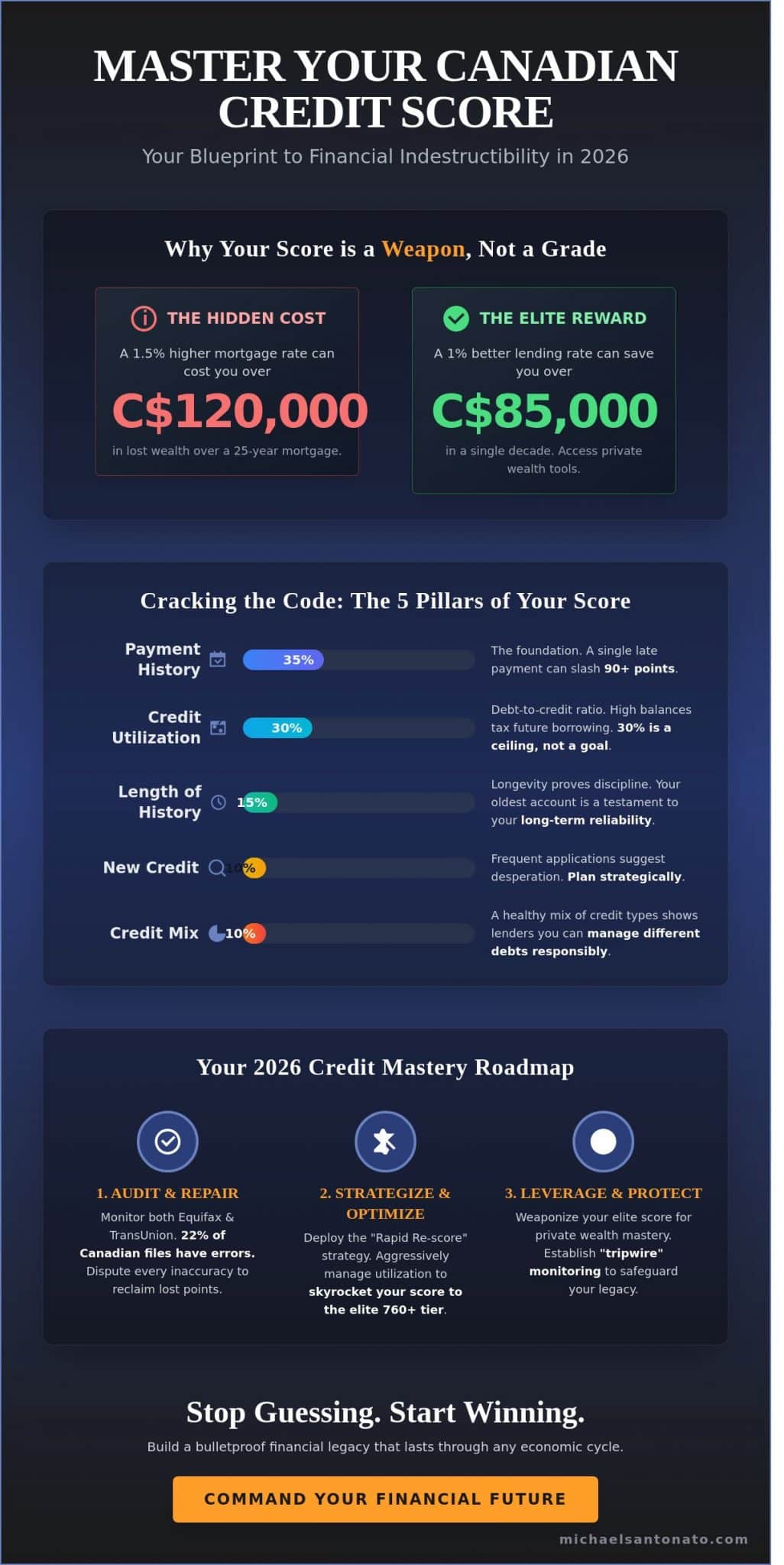

Your credit score isn’t a grade; it’s a weapon. Most people treat their financial standing like a passive observer, but in 2026, being a spectator is the fastest way to kill your legacy. Why settle for mediocrity when a 760+ credit score canada can slash your borrowing costs? A single percentage point difference in lending rates can cost a Canadian investor over C$85,000 in lost wealth over a decade. You’ve felt the frustration of watching your numbers fluctuate without logic or the anxiety of a lender saying “no” when you were ready to scale. It’s time to stop guessing and start winning.

I know you’re tired of the “black box” games played by the big banks. You want the breakthrough that comes with elite lending rates and private banking access. This guide is your blueprint for total mastery. I’ll show you how to rebuild your foundation and use your credit as a strategic asset for wealth protection. We’re moving beyond survival. We’re going to install the Financially Indestructible framework so you can command the market on your own terms.

Key Takeaways

- Stop viewing your credit as a mere number and master it as a high-performance reputation index essential for financial indestructibility in the 2026 Canadian economy.

- Deploy the “Rapid Re-score” strategy to aggressively purge zombie debts and skyrocket your credit score canada to the elite 760+ tier.

- Weaponize your credit to bridge the gap into private wealth mastery, using high limits to fuel Infinite Banking strategies and legacy-building assets.

- Establish a professional-grade maintenance roadmap and “tripwire” monitoring system to safeguard your wealth from inaccuracies and modern identity threats.

The Foundation of Financial Indestructibility: What Your Canadian Credit Score Really Means in 2026

Your credit score canada isn’t just a three-digit number generated by a computer. It’s your financial reputation index. In 2026, this number dictates your level of freedom and your ability to command respect in the marketplace. If you want to achieve Financial Indestructibility, you need more than a “passable” score. You need a weapon. Most people treat credit as a safety net. They use it to survive. They borrow to cover gaps in their lifestyle when the bank account hits zero. That ends today. We are shifting the paradigm from borrowing to survive to leveraging to thrive. You use credit to acquire assets, not liabilities. You use it to build a legacy, not a mountain of consumer debt. Ask yourself right now: Is your score an asset that accelerates your growth, or is it a liability holding you back from your true potential?

The 2026 Credit Landscape in Canada

The economic climate has shifted significantly. With interest rates hovering at higher levels than the 2010s average, lenders have tightened their requirements. A score of 700 used to be “good.” In 2026, that’s the bare minimum for basic approval. To access the lowest rates and the most powerful financial tools, you must aim for the 800+ elite tier. This isn’t about vanity; it’s about math. A 1.5% difference in a mortgage rate can save you over C$120,000 over a 25-year amortization. The Financial Consumer Agency of Canada (FCAC) provides the framework for your rights, but you must be the one to enforce them. Mastery requires constant vigilance.

Credit Score vs. Credit Report: Knowing the Difference

Think of your credit report as your history book. It records every financial move you’ve made over the last six years. Your score is your trajectory. It’s a prediction of your future performance based on that history. You cannot fix a score without auditing the report first. Errors are rampant. Data from early 2026 shows that roughly 22% of Canadian credit files contain inaccuracies that drag scores down. You must monitor both to ensure no ghosts from the past are sabotaging your future. Understand the mechanics of inquiries too. Soft inquiries for monitoring don’t touch your momentum. Hard inquiries for new applications can stall your progress if you aren’t strategic. Protect your momentum at all costs.

Cracking the Code: How Credit Scores are Calculated in Canada

Your credit score is not a mystery; it is a mathematical reflection of your financial integrity. To achieve financial mastery, you must understand the five pillars that define your credit score canada ranking. If you want to scale your wealth, you cannot afford to ignore these mechanics. Lenders in 2026 use advanced AI-driven models, but the core fundamentals remain unchanged. Stop treating your credit like a secondary thought. It is the engine of your financial growth.

- Payment History (35%): This is the foundation of your reputation. A single 30-day late payment can slash 90 points off your score in the current Canadian market. It’s non-negotiable. Consistency is the only path to a breakthrough.

- Credit Utilization (30%): This measures your debt-to-credit ratio. Carrying high balances is a tax on your future borrowing power. High-performers keep this number lean.

- Length of History (15%): Longevity proves discipline. Your oldest account is a testament to your long-term reliability and persistence. Don’t close old accounts just because you don’t use them.

- Public Records (10%): Bankruptcies, consumer proposals, or collections are massive red flags. They signal a lack of control to every lender in the country.

- Inquiries (10%): Frequent credit applications suggest desperation. High-performers don’t beg for credit; they command it through strategic planning.

Equifax vs. TransUnion: The Two Giants

Why is your score different on each platform? Equifax and TransUnion use proprietary algorithms that have evolved significantly by 2026 to include trended data and alternative payment history. Most major Canadian lenders, such as Scotiabank or BMO, might favor one bureau over the other for specific products. You must monitor both. If you spot a discrepancy, don’t panic. Dispute it immediately with documented proof. You are the CEO of your financial data. Mastery requires vigilance over every detail. This is how you build a bulletproof financial legacy that lasts through any economic cycle.

The Utilization Myth: Why 30% is the Ceiling, Not the Goal

Stop listening to average advice. Many people think 30% utilization is “good.” It isn’t. In the 2026 lending environment, 30% is the bare minimum to avoid a penalty. Credit utilization is the ratio of your outstanding balances to your total available credit limits. If you want a breakthrough score, aim for under 10%. For high-volume business spenders, the secret is making multiple payments throughout the month. Pay your balance three days before the statement date. This “hides” your spending from the bureaus and keeps your profile looking pristine even when you are moving C$50,000 in monthly volume. Results require strategy, not just effort.

The Breakthrough Strategy: How to Repair and Skyrocket Your Score Fast

Stop playing defense with your finances. Your credit score canada is a financial weapon, but if it’s riddled with inaccuracies, it’s a weapon pointed at your own legacy. You must hunt down “zombie” debts. These are old, settled, or flat-out incorrect entries that continue to bleed your points every single month. Statistics from consumer advocacy groups suggest that up to 25 percent of Canadian credit reports contain errors that negatively impact scores. You aren’t just looking for mistakes; you’re conducting a forensic audit of your financial life.

Adopt a “Rapid Re-score” mindset. While bureaus typically update every 30 to 45 days, you don’t have to wait for the slow grind of the system. If you’ve paid down a massive balance or cleared a collection, demand a mid-cycle update. This is about forcing the bureaus to recognize your reality now, not next month. Negotiate with your creditors from a position of power. Don’t beg for a break. Instead, offer a “pay for delete” or a settlement that ensures the account is marked as “paid in full.” Get every agreement in writing before a single cent leaves your bank account.

The final step to financial indestructibility is the “Indestructible” habit. Automate every single minimum payment. Missing a payment by even 24 hours can tank a 800-point score by 100 points instantly. Set the floor so you never fail, then manually pay the rest to crush the principal.

Disputing Errors Like a Professional

Precision is your best ally when fighting Equifax and TransUnion. Start by pulling your free consumer disclosure reports. Don’t just use an app; get the full file. When you find an error, file a formal dispute online or via registered mail. Registered mail is the “pro move” because it creates a legal paper trail that bureaus cannot ignore. If they refuse to remove a confirmed error after 30 days, escalate. Contact the provincial consumer protection agency or the Ombudsman for Banking Services and Investments. Discipline in your documentation will win the war of attrition every time.

Strategic Debt Restructuring

Debt isn’t always the enemy; poorly managed debt is. If high-interest credit card balances are suffocating your utilization ratio, you need a tactical shift. Using debt consolidation canada strategies allows you to move high-interest burdens into a lower-interest loan, immediately dropping your revolving utilization and spiking your score. Whatever you do, do not close your oldest accounts. Your “oldest” card represents your credit longevity. Closing it is like deleting years of your financial history. Keep it open, keep it active, and let it act as the anchor for your 2026 mastery plan.

Weaponizing Your Credit: From Good Score to Private Wealth Mastery

Stop treating your credit score like a vanity metric. It isn’t a trophy to put on a shelf; it’s a high-caliber tool for wealth creation. Most people in this country think a high score is just about shaving a few points off a mortgage. They’re thinking small. A 760+ credit score canada is actually your entry ticket to the big leagues of private finance. It represents the difference between being a consumer who pays interest and a capitalist who collects it.

The wealthy understand a fundamental truth: there’s a massive gap between consumer debt and strategic leverage. Consumer debt is what happens when you use a credit card to buy a C$3,000 television that loses half its value before you get it home. Strategic leverage is using a low-interest line of credit to fund an asset that generates cash flow or builds equity. One makes you a slave to the bank; the other makes the bank your junior partner. If you want to be financially indestructible, you must learn to use the bank’s money to buy assets while they’re still on sale.

Credit as a Gateway to the Infinite Banking Concept

Your credit profile is the engine room for infinite banking canada. To become your own banker, you need to minimize friction. A top-tier score ensures you get the most favorable terms on policy loans and external lines of credit. This allows you to fund high-cash-value whole life insurance policies with maximum efficiency. You aren’t just “borrowing” money. You’re executing a tactical shift. See your credit limit as your “opportunity fund.” When a deal hits your desk, you don’t wait weeks for a bank’s permission. You pull the trigger immediately because your reputation is already proven.

Building Corporate Credit for Business Owners

If you’re a business owner, your personal credit is the “pump primer” for your corporate legacy. You use your personal credit score canada standing to secure those first critical business lines. This is a strategic move, not a permanent state. The goal is the breakthrough moment where your corporation stands on its own financial feet. By separating personal and business liabilities, you protect your family’s future from the risks of the marketplace. You’re building a fortress. Once your business credit is established, you can scale with purpose without putting your personal assets on the line.

Are you ready to stop being a spectator and start building a legacy? Connect with me today to master your financial destiny.

Your 2026 Credit Mastery Roadmap: Protecting Your Legacy

You’ve built the foundation. Now you defend it. Your credit score canada isn’t a static number; it’s a living reflection of your financial integrity. High-performance professionals treat their credit like a high-performance engine. You don’t wait for the check engine light to flash before you look under the hood. You perform preventative maintenance to ensure peak operation at all times.

Commit to a monthly maintenance checklist. This is the discipline that separates the masters from the amateurs. Every 30 days, you must audit your accounts. Verify that every payment is recorded correctly. Ensure your credit utilization remains below 10% on every individual revolving line. If you see a balance creeping up, crush it immediately. This level of scrutiny ensures your financial reputation remains bulletproof.

Setting up “tripwires” is your next move. Use credit monitoring as an early warning system for identity theft. In 2023, the Canadian Anti-Fraud Centre reported over C$567 million in losses due to fraud. You can’t afford to be a statistic. Tripwires trigger real-time alerts for new inquiries or address changes. If someone tries to hijack your legacy, you’ll know within seconds. Never “set it and forget it” with your finances. That’s a trap for the complacent. Mastery is a journey, not a destination; keep pushing for impact.

Tools for Continuous Monitoring

Differentiate between free tools and premium protection. Equifax Complete Premier offers C$1 million in identity theft insurance and daily scans. TransUnion CreditView, often provided through banks like RBC or Scotiabank, offers a great baseline for score tracking. Check your full report at least once per quarter. Read the fine print in every alert. A minor “change in file” could be the first sign of a sophisticated breach. Stay ahead of the curve by analyzing the data, not just glancing at the score.

Commit to Financial Indestructibility

Stop settling for “average” credit. An average credit score canada is a ceiling on your life. It limits your leverage and increases your costs. You’re here to build something that lasts. This requires a shift from passive observation to aggressive management. It’s time to integrate your credit mastery into a comprehensive wealth plan that secures your future and your family’s legacy.

Don’t leave your success to chance. Book a strategy session to align your credit power with your long-term goals. The path to breakthrough starts with a single, decisive action. Take that step now.

Ready to dominate? Join the Financially Indestructible Program today and start scaling with purpose.

Take Command of Your Financial Legacy

Your credit isn’t just a three digit number on a screen; it’s the primary engine of your financial legacy. We’ve decoded how the 2026 landscape demands a shift from passive monitoring to the aggressive weaponization of your assets. You now have the roadmap to understand how a credit score canada is calculated and the exact strategies needed to skyrocket your standing fast. Knowledge alone won’t build your empire. Execution will.

I’ve spent over 10 years mastering the complexities of Canadian debt restructuring and implementing the Infinite Banking Concept for high achievers. As the founder of the Financially Indestructible framework, I’ve proven that financial sovereignty is a choice, not a matter of luck. Why continue playing defense with your capital when you can master the mechanics of private wealth? Stop waiting for the market to shift and start dictating your own terms. Your breakthrough is waiting on the other side of this decision.

Master Your Wealth with the Financially Indestructible Program

You have the tools and the strategy. Now, go out there and build something that lasts.

Frequently Asked Questions

What is considered a “good” credit score in Canada for 2026?

A credit score canada of 760 or higher is the current benchmark for financial mastery and the lowest interest rates. While 660 is the traditional baseline for a “good” rating, elite lenders now prioritize scores above 725 for premium products. High achievers aim for 800 plus to ensure total borrowing power. Don’t settle for average when excellence is within reach.

How often does Equifax and TransUnion update my credit score?

Equifax and TransUnion typically update your files every 30 to 45 days. This timeline depends on when your individual lenders transmit data to the bureaus. Some institutions report on the first of the month, while others use your specific billing cycle date. Consistency is key; track your progress monthly to catch discrepancies early and maintain your momentum.

Will checking my own credit score lower it?

Checking your own credit score is a soft inquiry and will never lower your score. It’s a common myth that holds people back from taking ownership of their financial destiny. You should monitor your report weekly through free tools or banking apps. This transparency allows you to spot errors and identity theft before they sabotage your legacy.

How long does it take to see a breakthrough in my credit score after fixing an error?

You will typically see a breakthrough in your score within 30 to 90 days after a dispute is resolved. Once the bureau verifies the correction, they update your file in the next reporting cycle. Speed is a competitive advantage here. If you don’t see a shift after 60 days, follow up immediately to ensure your progress isn’t stalled by administrative friction.

Can I buy a house in Canada with a credit score under 600?

You can buy a house with a score under 600, but you’ll pay a premium for the privilege. Traditional lenders like the Big Five banks usually require 680 for the best rates. You’ll likely need a B-lender or a private mortgage with interest rates 2% to 5% higher than the market average. Take action now to repair your score and save thousands in interest.

What is the fastest way to increase my credit limit without a hard inquiry?

The fastest way to boost your limit without a hard inquiry is to accept a pre-approved offer through your online banking portal. Banks often run internal audits every 6 months to identify low-risk clients. If you see a notification for a limit increase, click accept immediately. This lowers your credit utilization ratio instantly, which is a high-impact move for your credit score canada.

Does my income affect my credit score calculation?

Your annual income has zero impact on the mathematical calculation of your credit score. The bureaus care about your reliability and debt management, not the size of your paycheck. However, lenders will look at your Gross Debt Service ratio separately when you apply for a loan. Mastery of your credit is about behavior, not just your earnings.

How do I remove a consumer proposal or bankruptcy from my credit report early?

You cannot legally remove a consumer proposal or bankruptcy from your report before the regulated purge date. A consumer proposal stays for 3 years after your final payment. A first-time bankruptcy remains for 6 to 7 years after discharge depending on your province. Focus on building new, positive trade lines immediately to dilute the impact of past setbacks and rebuild your financial authority.