How much longer are you going to let the Big Five banks dictate the terms of your success? If you’re tired of watching 7.2% interest rates on business loans and 50% tax brackets cannibalize your hard-earned capital, it’s time for a radical shift. You already know that the current system is designed to keep you dependent on lenders who don’t care about your legacy. You want total control over your cash flow and a way to grow your wealth without the tax man taking a massive cut every year. This is where mastering infinite banking canada strategies becomes your ultimate competitive advantage.

In this 2026 guide, I’m going to show you exactly how to reclaim the banking function, bypass traditional lenders, and build a tax-efficient legacy that lasts. We’ll dive into the mechanics of using high-cash-value life insurance to create a repeatable system for financing C$100,000 purchases while your money continues to compound. It’s time to stop being a slave to the bank and start mastering your own financial destiny.

Key Takeaways

- Stop letting Canadian banks profit off your hard-earned deposits and learn how to reclaim the banking function to fuel your own growth.

- Master the mechanics of infinite banking canada by leveraging a specially designed life insurance policy as your own private, high-performance vault.

- Break free from the RRSP “tax time bomb” and the limitations of TFSAs to build a wealth structure that scales without government-imposed ceilings.

- Discover why 99% of agents structure policies incorrectly and how to use the PUA rider to accelerate your cash value for a true financial breakthrough.

- Secure your family’s legacy by learning how to “be the bank” for your children’s major milestones, ensuring multi-generational financial indestructibility.

Why Traditional Canadian Banking is Rigged Against Your Success

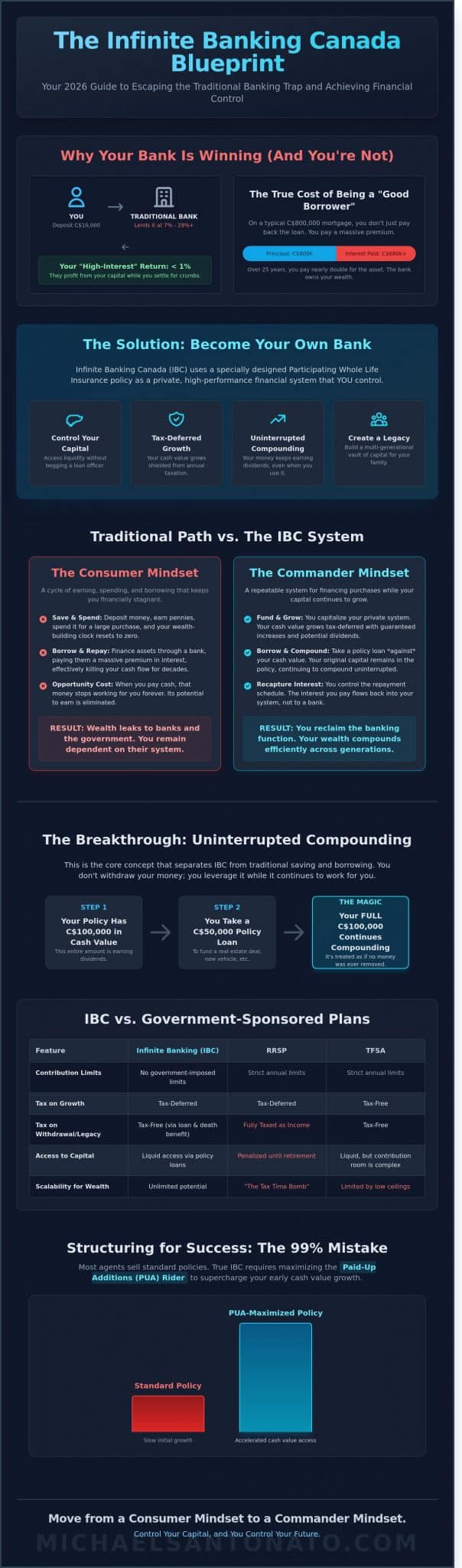

Wake up. Your local bank manager isn’t your partner. They’re a salesperson for a multi-billion dollar machine designed to extract wealth from your hard work. When you deposit C$10,000 into a savings account, the bank pays you less than 1% in interest. Then, they immediately lend that same capital to your neighbor at 7%, 12%, or even 29% on a credit card. They’re using your money to build their empire while you settle for crumbs. This is the hard truth of the Canadian financial system. You’re the one taking the risk, but they’re the ones reaping the rewards.

You need to stop being the victim in this transaction. The breakthrough isn’t finding a “better” bank. It’s becoming the bank. This is where infinite banking canada strategies change the game for individuals across the country. You’re adopting the blueprint laid out by Nelson Nash, creator of the Infinite Banking Concept, to reclaim the interest and profit that currently leaks out of your household. Most people are trapped in a loop of mediocrity. You save for a down payment, spend it, and start back at zero. Or you borrow from a lender and spend decades paying them back plus a massive premium. Both paths keep you stagnant. To win, you must own the process of financing, not just the financial products the big five banks push on you.

The Problem with Being a “Good Borrower”

Being a “good borrower” in Canada is a trap designed to keep you in debt. You’re celebrated for a high credit score just so institutions can lend you more. Interest volume is the silent killer of your wealth. On a C$800,000 mortgage at 5.5%, you’ll pay over C$680,000 in interest alone over 25 years. That’s nearly double the original price of the asset. With 47% of Canadian mortgages facing renewal in 2026, the “payment shock” is going to be a wake-up call for many. You’re also losing the “opportunity cost” every time you pay cash for an asset. Once that cash leaves your hand, it stops working for you forever. You’ve killed its ability to earn.

The Mindset of Financial Indestructibility

Stop chasing 8% returns in a volatile market while you’re losing 15% to interest, fees, and taxes. That’s a losing game. A capitalist mindset focuses on control and liquidity. You don’t need a better mutual fund. You need a system that gives you guaranteed access to capital without begging a loan officer for permission. This is about building a legacy that lasts. A properly structured infinite banking canada system doesn’t just fund your next investment property. It creates a multi-generational vault that provides certainty in an uncertain economy. Move from a consumer mindset to a commander mindset. Control your capital, and you control your future.

The Mechanics of Infinite Banking Canada: How the System Works

Stop treating your capital like a passive observer in someone else’s game. Most Toronto investors hand their hard-earned C$ to a bank, settle for a measly 1% interest rate, and then pay that same bank 7% to borrow their own money back. That is a losing strategy. To win, you must own the system. In the context of infinite banking canada, you aren’t just a customer; you’re the board of directors. You use a specially designed Participating Whole Life Insurance policy to build a private vault that grows regardless of what happens on Bay Street.

The Participating Whole Life Engine

Term insurance is a rental agreement that expires when you likely need it most. Universal Life is often a gamble on market volatility that can leave your legacy exposed. Neither works for this strategy. You need the stability of a participating policy from a major Canadian mutual insurer. These companies have paid dividends every single year since the late 1800s, providing a bedrock of certainty in an uncertain world. Cash Value is the liquid portion of your death benefit available for use. This pool of capital grows tax-deferred, shielded from the tax man and creditors alike. Unlike a standard savings account, this “vault” is guaranteed to increase every year you hold the policy.

The Uninterrupted Compounding Breakthrough

The real magic happens when you stop spending your money and start financing your life. Understanding how infinite banking works requires a shift in perspective. When you need capital for a real estate deal or a new vehicle, you don’t withdraw the cash. You take a policy loan against your death benefit. Your C$50,000 in cash value stays in the policy, earning dividends on the full amount even while you use the loan to fund an outside investment. This is uninterrupted compounding. It’s the ultimate math hack.

- No Credit Checks: You are the lender; the insurance company doesn’t care about your credit score.

- Flexible Repayment: You set the terms, allowing you to manage cash flow during lean months.

- The 2026 Advantage: With inflation projected to stay sticky through 2026, this system acts as a “Financially Indestructible” hedge, ensuring your purchasing power doesn’t erode.

If you want to stop being a slave to traditional lending cycles, you need to master your financial legacy by taking control of the banking function in your life. This isn’t about getting rich quick. It’s about building a fortress around your wealth. By using infinite banking canada, you ensure that every dollar you earn does two jobs at once. Why would you ever settle for a dollar that only works for the bank when it could be working for your family?

IBC vs. RRSPs and TFSAs: Breaking the Canadian Tax Trap

Stop playing small with your wealth. Most Toronto investors are walking straight into a trap. They believe the RRSP is the ultimate win because of the upfront tax deduction. It isn’t. You’re simply deferring taxes to a future where rates will likely be higher. When you hit age 71 and your RRSP converts to a mandatory RRIF, that tax time bomb explodes. You’re forced to take minimum withdrawals, and the CRA takes their cut before you see a cent. Is that true financial freedom? No. It’s a partnership with the government where they own the majority share.

TFSA limits are another bottleneck. A C$7,000 contribution limit for 2024 is a rounding error for a serious entrepreneur building a legacy. You need a bigger engine to drive your growth. This is why infinite banking canada is the essential “Third Bucket” for high-performers. It provides the tax-sheltered growth of an RRSP and the tax-free access of a TFSA without the restrictive annual caps. You aren’t limited by government-mandated ceilings; you’re limited only by your own ambition.

The Tax-Free Wealth Planning Advantage

CRA Section 148 is your best friend. It governs how life insurance is taxed, allowing your cash value to grow inside the policy without an annual tax bill. You aren’t just saving money; you’re building a private fortress. By using life insurance as a source of liquidity, you access capital through policy loans rather than withdrawals. These loans aren’t taxable events. This is the core of the Tax-Free Wealth pillar in the Financially Indestructible program. You maintain mastery over your capital while it continues to compound at a guaranteed rate.

Liquidity and Control Comparison

Pulling money from an RRSP before retirement triggers a withholding tax of up to 30%. That is a massive hit to your momentum. In contrast, IBC offers total flexibility and control. Business owners in the GTA are already ditching traditional bank lines of credit to finance C$150,000 equipment purchases through their own policies. They pay themselves back with interest, keeping the profit in their own ecosystem. This strategy also secures your legacy. Unlike an RRSP, which can be taxed at nearly 54% upon death in Ontario, your death benefit is paid out to beneficiaries entirely tax-free. You win during your life, and your family wins after you’re gone.

Implementing the System: How to Structure Your Private Bank

Most insurance agents will kill your wealth before it even starts. That is the cold, hard truth. Roughly 99% of agents in Canada structure policies to maximize their own commissions rather than your liquidity. They sell you a standard death benefit policy where your cash is locked away for a decade. If you want to master infinite banking canada, you must flip the script. You need a policy engineered for maximum cash value from day one. This requires a surgical focus on the Paid-Up Additions (PUA) rider. This rider is the fuel for your private bank; it allows you to overfund the policy, cramming in extra capital that goes straight to your accessible cash value instead of just buying more base insurance.

Determining your “Banking Capacity” is your first move. This isn’t a guess. It is a calculation of your current cash flow. If you are an investor moving C$5,000 a month into traditional savings or debt payments, that is your capacity. You aren’t spending more; you’re just changing the destination of that C$60,000 per year. The process is a disciplined four-step strike: a deep-dive consultation to map your goals, custom engineering of the policy, the underwriting phase, and finally, the execution of your first policy loan to recapture interest from the banks.

Finding the Right Mutual Insurance Company

Ownership matters. You must avoid the “Big Bank” insurance arms. Why? Because they answer to shareholders who want profits at your expense. For a successful IBC strategy, you only work with Mutual insurance companies. In a mutual structure, you are the owner. You participate in the profits. We look for Canadian carriers with a 100-plus year dividend history, such as Equitable Life or similar participating providers. These institutions have survived world wars and depressions without missing a single dividend payment to their policyholders.

Structuring for Cash, Not Just Commission

A “Standard” policy is a liability for an investor. You need a “High Cash Value” structure. This means reducing the base premium to the bare minimum required by the CRA and maximizing the PUA. If your agent hasn’t mentioned the 10/90 or 20/80 split, they are building a retirement plan for themselves, not you. You can use the Financially Indestructible Program to audit your current plan and ensure it is optimized for growth. Be prepared for the capitalization phase. Years 1 to 5 are about building the foundation. You are capitalized and ready to strike when the market presents an opportunity.

Stop letting the big banks dictate your financial ceiling. It is time to take control of your capital and build a legacy that lasts for generations. Book your strategy session today and start building your private bank.

Mastering Your Legacy: The Path to Being Financially Indestructible

You aren’t just building a bank account. You’re building a dynasty. Using infinite banking canada as your foundation isn’t about a single transaction; it’s the ultimate tool for multi-generational wealth. Statistics show the average Canadian family will spend over C$250,000 on interest alone over their lifetime. That is capital leaking out of your family tree and into the pockets of bank shareholders. IBC allows you to capture that leak. You become the source of capital for your children’s education or their first Toronto property. Imagine your kids borrowing from the family bank at 5% instead of a commercial lender at 8%. The interest stays in your circle. It compounds for your heirs. This is how you move from being a consumer to being the financier of your own bloodline.

Scaling Your System

One policy is just the starting line. As your income grows, your banking needs grow with it. High-performance investors often add a second or third policy every 24 to 36 months to expand their total capital capacity. If you’re a business owner, this is your secret weapon for growth. You can finance C$60,000 in new inventory or cover a C$100,000 payroll gap during seasonal dips without ever filling out a loan application. You bypass the red tape. You eliminate the standard 14-day waiting period for credit approval. When you scale infinite banking canada, you aren’t just saving; you’re weaponizing your cash flow. The psychological breakthrough of never needing a bank’s permission again changes how you play the game. You move faster. You take bigger swings. You win more often.

Your Invitation to Mastery

General financial advice is a trap. It’s designed for the masses, not for leaders who demand excellence. You don’t need another generic blog post or a “top ten” list. You need a personalized strategy that accounts for your specific tax bracket and legacy goals. Most people get stuck in the “knowing” phase. They read the books but never pull the trigger because they fear the complexity. Michael Santonato helps you bridge that gap between theory and high-performance execution. It’s time to stop being a slave to the big banks and start owning the system. The difference between a 3% stagnant return and a structured IBC system over 30 years can mean millions of dollars for your estate. Don’t leave your legacy to chance. Book your Private Wealth Coaching session now.

Take Command of Your Financial Destiny Now

The traditional Canadian banking system wasn’t built for your prosperity; it was built for theirs. You’ve spent years watching your wealth get eroded by the RRSP tax trap and the structural limitations of the TFSA. It’s time to stop being a spectator in your own financial life. By mastering infinite banking canada, you seize control of the banking function and turn every C$1 you spend into a tool for multi-generational growth. I’ve spent over 10 years perfecting these high-cash-value policy structures to ensure they’re bulletproof. This isn’t about abstract theory. It’s about the pragmatic application of wealth mechanics that keep your capital liquid, tax-advantaged, and entirely under your command. You don’t need another “safe” investment; you need a system that makes you indestructible. My direct mentorship will bridge the gap between where you are and the legacy you’re destined to build. Your breakthrough starts the moment you decide to own the bank. Let’s stop playing the bank’s game and start playing yours.

Join the Financially Indestructible Program and Start Your Private Bank Today

You have the blueprint. Now you need the courage to execute. I’ll see you on the inside.

Frequently Asked Questions

Is Infinite Banking legal in Canada and approved by the CRA?

Yes, it is 100% legal and operates within the strict framework of the Canadian Income Tax Act. Specifically, Section 148 governs how life insurance policies grow tax-deferred. You aren’t dodging taxes; you’re using a government-approved vehicle to build a private reserve. Major Canadian carriers like Canada Life or Sun Life have offered these participating policies for over 175 years. It’s a proven strategy for those who want to stop giving their interest to the big banks.

How much money do I need to start an Infinite Banking system in Canada?

You can start with as little as C$500 per month, but I recommend C$1,000 or more to see real momentum. If you want to build a legacy, you have to fund it properly. Most successful Toronto investors I work with commit between C$12,000 and C$50,000 annually. This ensures the cash value grows fast enough to fund major purchases or investments within the first 24 to 36 months. Don’t play small if you want big results. If you’re ready to take the next step, learn how to build your infinite banking system in 2026 with a comprehensive strategy that puts you in complete control.

Can I use Infinite Banking for my Canadian small business?

Absolutely, and it is a game changer for your corporate balance sheet. By using a corporately owned policy, you can move “trapped” retained earnings into a tax-advantaged environment. This allows you to finance equipment, inventory, or expansion without begging a traditional lender for a loan. Business owners in Ontario use this to turn their expenses into assets. It’s about taking control of your capital and keeping the interest inside your own ecosystem.

What happens if I can’t pay back a policy loan?

Your credit score stays untouched because you are the banker. If you don’t pay back the loan, the outstanding balance plus interest is simply deducted from the total death benefit when you pass away. However, failing to repay means you’re stealing from your own future. To achieve true financial mastery, you should treat your policy with more respect than a traditional bank. Pay yourself back to keep your infinite banking canada strategy growing at maximum velocity.

How does Infinite Banking compare to a HELOC (Home Equity Line of Credit)?

A HELOC is a debt trap controlled by the bank; a policy loan is an asset you control. Banks can freeze or call in your HELOC at any time, as seen during the 2008 financial crisis. With a Whole Life policy, your access to cash is guaranteed by the contract. Plus, your policy continues to earn dividends on the full amount, even if you’ve borrowed against it. A HELOC doesn’t pay you to borrow your own equity.

Is the growth in a Whole Life policy guaranteed?

Yes, your policy includes a contractually guaranteed cash value increase every single year. While the dividend portion isn’t guaranteed, major Canadian mutual insurers have paid dividends every year since the late 1800s. This isn’t a speculative play like crypto or volatile tech stocks. It is a slow, steady, and predictable climb toward wealth. You get a floor of safety that ensures your foundation never cracks, no matter what the TSX does.

Can I use Infinite Banking to pay off my mortgage faster?

You can use your cash value to crush your mortgage years ahead of schedule. By redirecting your savings into a policy first, you build a liquid pool of capital. Once that pool is large enough, you make a massive C$50,000 or C$100,000 principal payment. This move wipes out years of interest payments. It’s about velocity. You’re using the same dollar to grow your wealth and eliminate your debt simultaneously. It’s the ultimate financial double-play.

How long does it take to see significant cash value in my policy?

You will see accessible cash within the first year, but the real “break-even” point usually hits between years 4 and 7. This is a long-term play for serious high-performers, not a get-rich-quick scheme. By year 10, your annual cash value growth often exceeds your annual premium. That’s the moment your infinite banking canada system becomes a self-sustaining wealth engine. Patience in the early years builds the empire you’ll enjoy for decades.