How much of your hard-earned wealth are you handing over to a bank that doesn’t care about your legacy? Right now, the average Canadian household owes C$1.76 for every dollar of disposable income. That is a staggering amount of interest leakage draining your potential before you even see it. You feel the weight of these payments every month; you see the tax man waiting to take his cut of your retirement; and you are tired of asking for permission to use your own capital. It is time to stop playing by their rules and start playing by yours through the power of infinite banking.

I am here to show you exactly how to fire your bank and reclaim your financial sovereignty. We are not talking about theory; we are talking about a pragmatic shift that allows you to finance major purchases without a credit check and build a tax-free mountain of wealth. This article breaks down the specific mechanics of high cash value policies and the strategic mindset required to dominate your financial future in 2026. Get ready to stop being a debtor and start being the bank.

Key Takeaways

- Stop the “Great Banking Heist” by identifying the interest leakage bleeding your C$ cash flow and learn how to redirect that lost capital back to your own balance sheet.

- Master the specialized design of infinite banking to transform dividend-paying whole life insurance into a powerful, tax-efficient engine for liquid wealth and legacy.

- Break free from the RRSP tax time bomb and understand why “deferred” taxes are a high-risk partnership that gives the government control over your future retirement.

- Execute a five-step tactical roadmap to audit your current finances and build a private banking system that ensures you never have to beg a traditional bank for a loan again.

- Learn why the “Financially Indestructible” coaching framework is the essential catalyst to shift your mindset from a consumer to a high-performance wealth creator.

The Great Banking Heist: Why Your Current Strategy is Bleeding You Dry

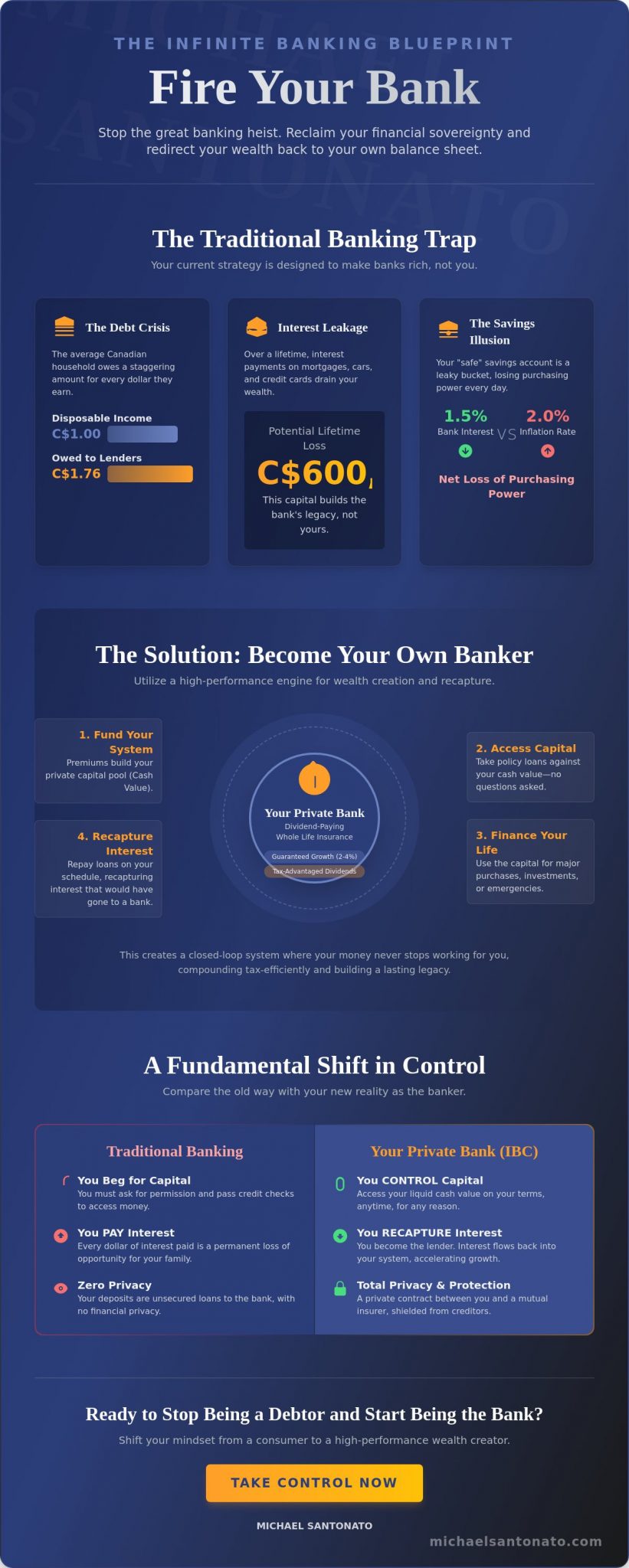

You’re being robbed in broad daylight. Every month, you grind for a paycheck only to hand the lion’s share back to the Big Five banks. It’s a cycle of financial dependency that most Canadians accept as “normal.” But it isn’t normal; it’s a heist. The truth is that your current financial strategy is designed to benefit the institution, not the individual. Infinite banking is the breakthrough you need to stop the bleeding. It’s the process of using dividend-paying whole life insurance to finance your own life, business, and major purchases. This isn’t a new gimmick. The concept was pioneered by R. Nelson Nash, who realized that the problem isn’t how much you earn, but who controls the pool of capital. Right now, you’re hemorrhaging cash through interest leakage. You’ll lose hundreds of thousands of C$ over your lifetime to third-party lenders. Why are you working for the bank when your money should be working for you?

The Illusion of the ‘Safe’ Savings Account

Your C$50,000 sitting in a traditional savings account is dying a slow death. With the Bank of Canada targeting a 2% inflation rate and most banks offering less than 1.5% interest before taxes, you’re losing purchasing power in real-time. Traditional commercial banking offers zero privacy and even less control. Your deposits are essentially unsecured loans to the institution. It’s time to stop settling for the crumbs they leave behind. Infinite banking is financial sovereignty in a box. It eliminates the middleman and puts you back in the driver’s seat of your own economy.

Interest: The Silent Wealth Killer

The average Canadian professional is on track to pay over C$600,000 in interest alone throughout their career. Consider the interest on a C$500,000 mortgage, the financing for a C$70,000 SUV, and the high-interest credit used for business growth. That’s capital that could have built your legacy. Instead, it built the bank’s skyscraper in downtown Toronto. When you choose to become the lender, you capture that interest instead of paying it out to a stranger. You redirect the flow of wealth back into your own ecosystem. If you’re ready to stop the theft and see the raw truth about your balance sheet, it’s time for The Wake Up Call course. Mastery requires a shift in perspective. Are you ready to scale with purpose and reclaim your impact?

- Stop Interest Leakage: Reclaim the hundreds of thousands currently leaving your pocket.

- Control the Velocity: Keep your money moving and working for you, not the bank.

- Build a Legacy: Shift from a consumer mindset to a capitalist mindset.

The math doesn’t lie. Every dollar you pay in interest to a bank is a dollar that can never work for your family or your business again. It’s a permanent loss of opportunity. By implementing infinite banking, you create a system where you are both the borrower and the depositor. This is how you achieve high-level performance in your personal finances. It’s about more than just money; it’s about the freedom to operate without asking for permission from a loan officer.

The Engine of IBC: How Dividend-Paying Whole Life Insurance Actually Works

Forget everything you think you know about traditional life insurance. Most people see Whole Life as a slow, expensive dinosaur. That is because they are looking at off-the-shelf products designed by bankers to benefit the bank. To master infinite banking, we use a specialized policy design that prioritizes early cash value growth over a massive initial death benefit. This is a precision-engineered financial tool. It is not a passive savings account; it is a high-performance engine for wealth recapture.

Every policy has two gears: the guaranteed and the non-guaranteed components. In Canada, major mutual insurance companies provide a guaranteed floor, often around 2% to 4%. On top of that, you receive non-guaranteed dividends. Do not let that “non-guaranteed” label fool you. The top Canadian mutual insurers have paid dividends every single year for over 160 years. They stayed profitable through the Great Depression and both World Wars. This creates a breakthrough in your financial strategy by providing a stable, compounding environment that the volatile TSX simply cannot match.

The real magic happens through uninterrupted compound interest. When you understand Infinite Banking: Using Life Insurance as a Source of Liquidity, you realize your money never stops working for you. Even when you use your capital, the full amount stays in the policy, earning interest and dividends. This is how you achieve financial mastery. You are no longer losing the opportunity cost of your spending. Under Section 148 of the Canadian Income Tax Act, this growth occurs in a tax-exempt environment, and the final death benefit passes to your heirs tax-free. It is the ultimate legacy play.

Cash Value vs. Death Benefit: The Dual-Purpose Asset

Think of your cash value as a private vault. It is your liquid capital, accessible within days without a credit check or a dehumanizing bank interview. This is your “opportunity fund” for real estate or business expansion. While the cash value provides current liquidity, the death benefit ensures your impact lasts for generations. This is not “buy term and invest the difference.” That strategy forces you to rent your protection and gamble your savings in a rigged market. This is a Tier 1 asset class that provides both a living benefit and a permanent legacy. If you want to see how this fits your specific numbers, you can book a brief strategy session to review your goals.

The Power of Policy Loans

The mechanics of a policy loan are often misunderstood. You aren’t withdrawing your own cash. You are taking a loan from the insurance company and using your cash value as collateral. Because your money stays in the policy, the insurer continues to pay you dividends on the full, original amount. If you have C$100,000 in cash value and take a C$40,000 loan to buy equipment, you still earn dividends on the full C$100,000. Contrast this with an RRSP or 401(k) loan. Those systems force you to stop your growth, pay back the loan with after-tax dollars, and follow strict government timelines. IBC gives you total control over the repayment schedule, allowing you to scale your wealth with purpose and speed.

The Tax Time Bomb: RRSPs, 401(k)s, and the Myth of ‘Deferred’ Taxes

Most high achievers believe their RRSP is a growing asset. It isn’t. It’s a joint venture with the Canada Revenue Agency where they own an undisclosed percentage of your hard work. You take 100 percent of the market risk. You do all the labor. Yet, the government gets to decide their share of the harvest thirty years from now. It’s a partnership where one partner has the power to change the rules at any moment. Does that sound like a winning strategy to you?

The “pay later” model is a trap for anyone aiming for true wealth. We’re looking at a future where government debt is ballooning. When the bill comes due in 2026 and beyond, where do you think they’ll find the money? They’ll find it in your “deferred” accounts. If tax rates climb to 50 percent or higher, your retirement nest egg just got cut in half by legislative whim. This is why you need financial indestructibility. You must shield your capital from the shifting winds of politics. Do you want to be a tenant in your retirement, begging for your own money, or do you want to be the landlord?

The Liquidity Trap of Traditional Retirement Plans

RRSPs are cages for your capital. If you try to access your money to fund a business opportunity or handle a C$20,000 emergency before age 65, the system punishes you. You’ll face immediate withholding taxes that can reach 30 percent; that’s before you even calculate your final tax bill. Your money is held hostage when you need it most. Contrast this with infinite banking. When you use a high cash value life insurance policy, your liquidity is guaranteed. You don’t ask for permission. You don’t pay penalties. You use your capital to scale your business today while it continues to grow for tomorrow. This is the level of control required for a legacy. If you’re ready to break free, Get the Book to see how we structure these systems for maximum access.

Tax-Free Growth vs. Tax-Deferred Uncertainty

A tax-deferred account is a giant question mark. You’re betting that your tax bracket will be lower in the future, which is a losing bet for any ambitious professional. An Introduction to the Infinite Banking Concept explains how this strategy creates a predictable, tax-free outcome. By utilizing infinite banking, you’re creating a private pool of capital that grows regardless of what happens in Ottawa. The net effect on your legacy is massive. You aren’t leaving your heirs a tax bill; you’re leaving them a tax-free windfall. This is the ultimate hedge against a system designed to erode your purchasing power. Stop playing by their rules and start building your own bank at True Financial Education.

Mastering the Implementation: 5 Steps to Your Own Private Bank

Stop being a servant to the big banks. If you want to master infinite banking, you need a blueprint that works in the Canadian market. This isn’t a theory. It’s a mechanical process. Follow these five steps to take back control of your financial destiny and stop the wealth transfer to institutional lenders.

- Step 1: Audit your cash flow. Look at your bank statements. How much interest are you paying to lenders for your car, your mortgage, or your business equipment? That’s wealth leaking out of your family’s bucket. Identify every cent of C$ interest escaping your control.

- Step 2: Connect with a specialist. You can’t do this with a generic insurance agent. You need a specialist to design a high-cash-value, dividend-paying policy. If it’s not structured correctly from day one, it fails. You can grab my book to see exactly how these structures work for Canadians.

- Step 3: Capitalize your bank. This is the funding phase. You must fund the policy with purpose and discipline. You’re building the foundation of your legacy. This isn’t a bill; it’s a deposit into your own system.

- Step 4: Execute policy loans. Stop using traditional financing for major purchases. Use your policy to buy that C$60,000 truck or that real estate investment. You’re using your own capital while your original money continues to grow inside the policy.

- Step 5: Repay your bank. Treat your bank with respect. Repay the loan on your terms, but ensure you’re capturing that interest for yourself. This is how you win the game.

Designing the Policy for Performance

A standard whole life insurance policy won’t work for this strategy. Most off-the-shelf products are designed for death benefits, not cash growth. Your policy must be engineered for maximum early cash value. You need a mutual insurance company. Why? Because as a policyholder, you participate in the profits through dividends. Don’t expect instant gratification. The break-even point usually occurs between years 7 and 10. Patience is the price of financial mastery.

The Discipline of the Banker

Don’t fall into the easy money trap. Just because you can access the cash doesn’t mean you should spend it recklessly. You must act as both the lender and the borrower. If you wouldn’t let a stranger skip a payment to your bank, don’t let yourself off the hook. Paying yourself back with interest is the secret to accelerating your wealth. This is a lifelong strategy. It’s about building a multi-generational legacy, not a quick fix for a single year.

Are you ready to stop the interest drain and start building your own private reserve?

Breakthrough to Mastery: Why Coaching is the Catalyst for Financial Indestructibility

You have the policy. You have the math. Why do most people still fail to achieve total sovereignty? It is not the contract. It is the person holding the pen. The biggest hurdle to infinite banking isn’t a lack of capital; it’s a legacy of “borrower’s logic” that keeps you playing small. You cannot build a private bank while still thinking like a consumer who is afraid of debt. You need a total shift in your financial DNA.

Without a roadmap, Canadian professionals often fall into predictable traps. They underfund their policies or fail to treat their loans with the same respect they would give to a Big Five bank. This lack of discipline kills the compounding effect before it can truly take flight. My “Financially Indestructible” coaching framework provides the tactical guardrails you need. It ensures your C$ are moving with purpose, preventing the common mistakes of poor loan management and stagnant cash flow that plague the unguided.

From Theory to Impact

Knowing the mechanics of infinite banking is useless if you don’t pull the trigger. Busy executives don’t need more information; they need implementation. Professional coaching turns abstract concepts into a concrete cash flow strategy that fits your lifestyle. Having a strategic partner ensures you don’t miss opportunities to recapture interest that would otherwise leak out to external lenders. You gain the confidence to move large sums of capital with certainty. If you’re ready to stop theorizing and start building, explore the Financially Indestructible coaching program to bridge the gap between potential and performance.

Scaling Your Legacy with Purpose

True wealth is never a solo sport. It’s about building a system that outlives your current business cycle. You can scale this strategy across your entire family or business partnership, creating a pool of capital that serves generations. Imagine your children coming to the “Bank of Mom and Dad” for their first home or business startup, paying interest back into the family ecosystem instead of a commercial lender. This is how you stop the generational wealth drain. You aren’t just saving money; you’re teaching the next generation to be the banker, not the borrower.

Mastery isn’t found in a textbook. It’s forged through action under the guidance of someone who has already mastered the terrain. Your legacy won’t build itself through wishful thinking. Take ownership of your financial destiny today. Build a foundation that is truly indestructible and leave a mark that lasts forever.

Claim Your Financial Sovereignty Today

The traditional Canadian banking system is designed to keep you on a treadmill of debt and deferred taxes. By the time you realize your RRSP is a tax time bomb, it’s often too late. You’ve seen how infinite banking functions as a high-performance engine for your wealth, using dividend-paying whole life insurance to reclaim the interest you’re currently losing to big banks. This isn’t about minor tweaks; it’s about a total breakthrough in how you handle every C$ you earn.

Success requires more than just reading an article. It demands implementation and the kind of direct mentorship that comes from over a decade of real-world financial mastery. Michael Santonato specializes in high-performance coaching for Canadian professionals to move beyond theory and into results-oriented action. Don’t let your legacy be a footnote in a bank’s quarterly report. Take the lead, master your cash flow, and build a foundation that is truly indestructible.

Ready to become your own banker? Join the Financially Indestructible Coaching Program today.

Your journey to financial mastery starts with a single, decisive move. You have the tools and the vision. Now, let’s get to work.

Frequently Asked Questions

Is Infinite Banking just a scam using whole life insurance?

Infinite banking isn’t a scam; it’s a proven financial strategy utilizing dividend-paying whole life insurance from mutual companies that have operated in Canada since 1847. You aren’t buying a “get rich quick” scheme. You’re building a rock-solid foundation for your legacy. This process involves redirecting your cash flow to build an asset that grows tax-sheltered, providing you with a private source of capital that bypasses traditional lenders.

Can I use Infinite Banking if I have a low credit score?

You can absolutely start an infinite banking strategy with a low credit score because the insurance company doesn’t check your credit when you request a policy loan. Your cash value acts as the collateral. This is about reclaiming your sovereignty. When you become your own banker, you stop begging traditional institutions for permission to access your own capital. You set the terms and you control the timeline.

How much money do I need to start an Infinite Banking policy?

Most high-performing policies in Canada require a minimum commitment of C$500 to C$1,000 per month to ensure the growth is meaningful. This isn’t a hobby; it’s a commitment to your financial mastery. While some smaller policies exist, you need enough fuel to ignite the engine. If you want to see a breakthrough in your net worth by 2026, you must prioritize this capital allocation today.

Is Infinite Banking legal in both Canada and the United States?

Infinite banking is fully legal and regulated in both Canada and the United States under local tax codes. In Canada, these policies must comply with the Income Tax Act, specifically the “exempt test” which ensures the growth remains tax-advantaged. Major Canadian carriers have honored these contracts for over 175 years. It’s a legitimate path to financial freedom that elite families have used for generations to protect their impact.

Can I use my Infinite Banking policy to pay off my mortgage faster?

You can use your policy to pay off your mortgage faster by leveraging the cash value to make lump-sum payments against your principal. By doing this, you’re not just “spending” money; you’re moving it from one asset to another. This strategy recaptures interest that would otherwise go to a commercial bank. Why give your hard-earned Canadian dollars to a lender when you can keep that profit within your own family ecosystem?

What happens if I can’t make a premium payment one year?

If you miss a premium payment, your policy can utilize an “automatic premium loan” where the cash value covers the cost to keep the contract active. This isn’t a license to be lazy, but it provides a safety net during lean years. Most robust policies also offer a “premium offset” feature after the 7th or 10th year. It’s about building a resilient structure that supports your high-performance lifestyle, even during a temporary setback.

How long does it take for the cash value to become accessible?

You can typically access your cash value within the first 12 to 24 months of the policy’s life. While traditional whole life takes longer to “break even,” a properly structured policy is designed for early liquidity. You need access to capital to seize opportunities. Don’t wait decades for a breakthrough. Use this liquidity to fund business growth or investments that accelerate your journey toward total financial sovereignty.

Is the interest I pay on a policy loan tax-deductible?

Interest on a policy loan is only tax-deductible in Canada if you use the funds to earn income from a business or property. This falls under Paragraph 20(1)(c) of the Income Tax Act. If you use the loan for a personal vacation, it’s not deductible. If you use it to scale your business or buy a rental property, it becomes a powerful tool. Are you playing the game to win, or are you just spectating?