Are you actually building a legacy, or are you just acting as a high-paid tax collector for the CRA? In 2026, relying on traditional corporate investment strategies canada has become a dangerous game. With the federal tax rate on corporate investment income at 38.67% and the Small Business Deduction phasing out once your passive income hits $50,000, your surplus isn’t just sitting; it’s shrinking. You worked too hard for this capital to let a “Passive Income Tax Trap” dictate your financial future.

I know you’re tired of the market volatility and the high personal tax rates that hit every time you try to access your own money. It’s time to change the rules. This guide promises to show you how to stop the bleeding and transform your corporate surplus into a tax-efficient, liquid wealth engine. You’ll learn how to secure tax-free access to capital and build a structure that’s shielded from creditors. We’re going to master the shift from buying financial products to “becoming the bank” so you can achieve true financial indestructibility.

Key Takeaways

- Stop letting the “Passive Income Tax Trap” cannibalize your Small Business Deduction and learn to protect your hard-earned active business income.

- Master the mechanics of corporate investment strategies canada by shifting from traditional market-linked products to a structural “private vault” that guarantees liquidity.

- Unlock the secrets of the Capital Dividend Account to pull capital out of your corporation without triggering personal tax liabilities.

- Discover why high-performance entrepreneurs are ditching RRSPs for Individual Pension Plans to secure larger tax-deductible contributions and asset protection.

- Move beyond theory and execute a breakthrough by auditing your current wealth leaks to ensure your corporate surplus serves your legacy, not the CRA.

The 2026 Canadian Corporate Tax Trap: Why Your Retained Earnings Are At Risk

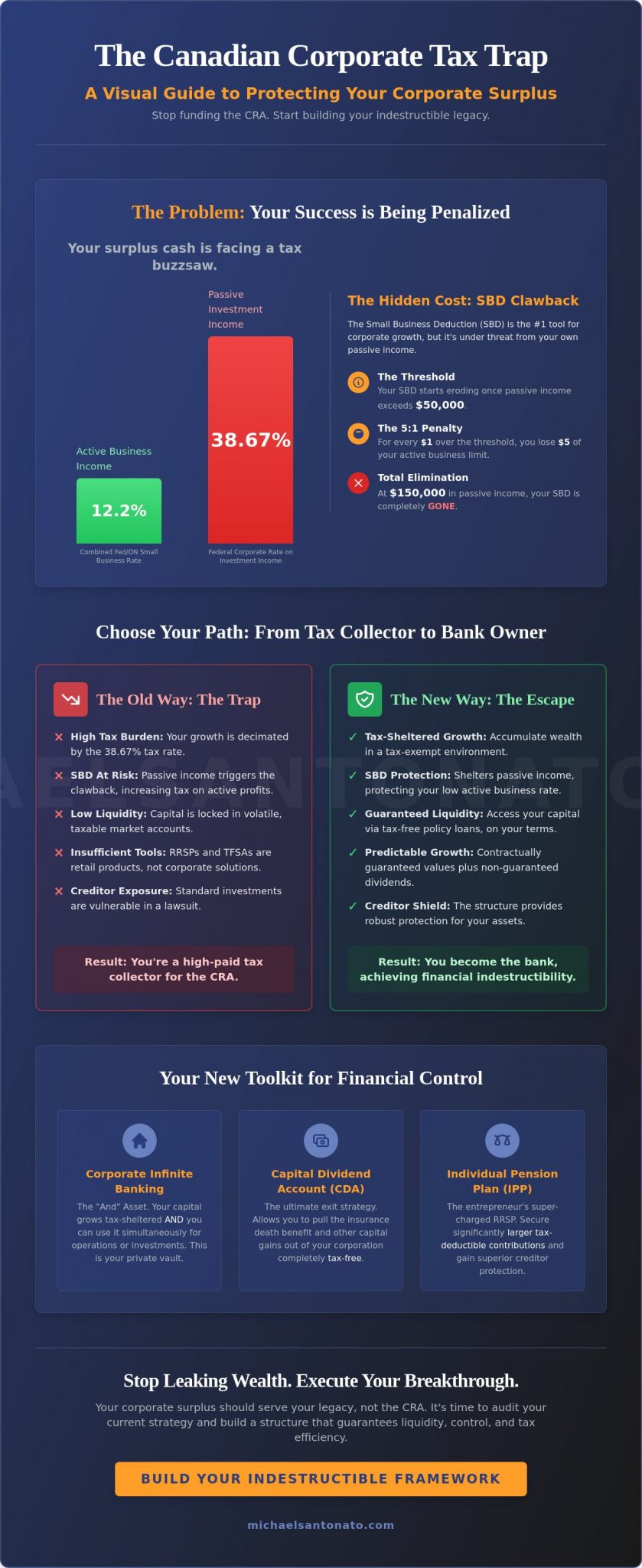

Your corporation is under attack. Most business owners think they’re winning because they had a profitable year, but if you’re holding excess cash in traditional accounts, you’re walking into a buzzsaw. The CRA has designed the Canadian corporate tax system to penalize your success through the Passive Income Tax Trap. In 2026, the federal corporate tax rate on investment income is a staggering 38.67%. Compare that to the combined federal and Ontario small business rate of 12.2%. That’s a massive gap. If you don’t rethink your corporate investment strategies canada, you’re handing over nearly 40% of your growth to the government before you even see a dime.

Playing it safe is the new high risk. You might think a GIC or a high-interest savings account is a “secure” place for your reserves. It’s not. When you factor in that 38.67% tax hit and the persistent inflation of 2026, your real rate of return is often negative. You’re literally losing purchasing power while your capital sits idle. This isn’t just about numbers; it’s about the psychological toll of watching your hard-earned surplus evaporate. You didn’t build this business to tread water. You built it to create a legacy, and that requires a strategy that protects your capital from predatory tax policies.

The Hidden Cost of the Small Business Deduction (SBD) Clawback

The math is brutal. Once your corporation earns more than $50,000 in passive investment income, the CRA starts clawing back your Small Business Deduction. For every $1 you earn above that $50,000 mark, you lose $5 of your $500,000 active business limit. It’s a 5:1 penalty. If you hit $150,000 in passive income, your SBD is gone. You’ll jump from a 12.2% tax rate to a 26.5% general rate on your hard-earned business profits. The SBD clawback is the #1 threat to corporate growth in Canada because it punishes the very capital you need to scale.

Why Traditional RRSPs and TFSAs Aren’t Enough for Business Owners

Retail bank advisors love to push RRSPs and TFSAs because it’s easy for them, not because it’s best for you. For a high-performing business owner, an RRSP is often a tax time bomb. You’re deferring tax today only to pay it at a potentially higher rate when you’re ready to enjoy your legacy. Plus, that money is trapped. What about TFSAs? The 2026 contribution limit is a mere $7,000. That’s pocket change for a serious corporation. You need corporate investment strategies canada that handle hundreds of thousands in surplus, not retail products that were never designed for the elite entrepreneur. Stop following standard advice if you want non-standard results.

Corporate Infinite Banking: The Ultimate Strategy for Liquidity and Control

Stop asking for permission. Most entrepreneurs spend their lives begging big banks for access to the very capital they worked so hard to earn. When you rely on standard corporate investment strategies canada, you’re playing a game where the house always wins. You lock your money in accounts you can’t touch, or you subject your reserves to market swings that keep you up at night. There’s a better way. It’s called the Infinite Banking Concept (IBC), and it’s not just “life insurance.” It’s a structural tool designed to give you total mastery over your cash flow.

Think of it as building a private vault within your company. By using a corporate-owned, participating whole life insurance policy, you create what I call the “And” Asset. Your money doesn’t just sit there. It grows through contractually guaranteed increases and dividends while you simultaneously use that same capital to fund your operations. While your competitors are stressed about the Bank of Canada’s rate holds, you’re operating with a predictability that only a contractually guaranteed system can provide. Mastery over cash flow is always more valuable than chasing an extra 1% yield in a taxable account. If you’re ready to see how this fits your specific business, you can book a discovery call to discuss your roadmap.

The Mechanics of the Infinite Banking Concept in Canada

This strategy relies on the strength of “mutually owned” insurance companies. Unlike traditional banks that answer to shareholders, these companies answer to you, the policyholder. Your corporate surplus earns dividends that have been paid out every single year for over a century. The magic happens through policy loans. You can access your cash value without triggering a taxable event or a CRA audit. Your original capital stays in the policy, compounding as if you never touched it. For a deeper dive into the technical details, check out my Infinite Banking Canada: The 2026 Guide.

Becoming Your Own Banker: Turning Expenses into Assets

Every time you buy equipment, a vehicle, or real estate, you’re either paying interest to a bank or losing the interest you could have earned elsewhere. This is a wealth leak. With IBC, you use the “Recapture” strategy. You finance these purchases through your policy and then pay the interest back to your own corporation instead of a Big Five bank. You’re turning a necessary business expense into a growing asset for your legacy. This is how you stop being a customer of the financial system and start becoming the bank. I encourage you to Get the Book to see the full framework of how this transformation works in real-time.

- Control: You decide the repayment terms, not a credit officer.

- Liquidity: Access capital within days, no questions asked.

- Certainty: Your growth is locked in, regardless of market volatility.

Traditional Corporate Investing vs. The Financially Indestructible Framework

Why settle for “average” when you can have certainty? Most advisors will tell you to dump your corporate surplus into a diversified portfolio of stocks and bonds and hope for the best. That’s not a strategy; it’s a gamble. When you compare traditional corporate investment strategies canada to a financially indestructible framework, the choice becomes obvious. Traditional investing leaves you vulnerable to market cycles. If the market drops 20% right when your business needs a capital injection, you’re stuck. You’re forced to sell at a loss or wait years for a recovery. Is that the kind of control you want over your legacy?

The differences in tax efficiency are even more staggering. In a traditional corporate account, your dividends and capital gains are subject to that 38.67% tax rate we discussed earlier. Within a specialized whole life policy, your growth is tax-free. You also avoid the nightmare of probate fees and heavy taxes on corporate shares upon your passing. Instead, the death benefit flows through the Capital Dividend Account to your heirs tax-free. You’re choosing between a system that leaks wealth at every turn and one that acts as a sealed, high-performance engine for your wealth.

The Fallacy of the ‘Low Fee’ ETF in a Corporate Account

Retail banks push low-fee ETFs as the ultimate solution for business owners. Don’t fall for it. A 0.2% management fee is completely irrelevant if you’re losing nearly half of your gains to the CRA. You’re also fighting “Sequence of Returns Risk.” If your portfolio takes a hit in the early years of your business expansion, the math of compounding breaks. You can’t scale a business on “average” returns that only look good on paper. You need real, accessible wealth that doesn’t disappear when the market gets moody. Stop following the herd toward mediocrity.

Asset Protection: Shielding Your Wealth from Creditors

Your brokerage account is a sitting duck. In a lawsuit-heavy world, traditional corporate investments are easy targets for creditors. A specialized whole life structure provides a unique layer of creditor protection under provincial insurance acts. You’re building a moat around your wealth. This structural mastery ensures that no matter what happens in the courtroom or the boardroom, your family’s future remains untouched. Why leave your most valuable assets exposed when you can secure them in a private, protected vault? It’s time to stop playing defense and start building a fortress.

- Guaranteed Growth: Contractual increases that don’t care about market crashes.

- Tax-Free Flow-Through: Move wealth to the next generation without the 50% haircut.

- On-Demand Liquidity: Access your capital in days, not years.

Advanced Tax Optimization: CDA, IPPs, and Strategic Salary Mix

Information without execution is just noise. You now understand how to protect your capital and build a private vault, but how do you actually get that money into your hands without the CRA taking a massive cut? This is where true mastery of corporate investment strategies canada separates the high-performers from the amateurs. You need a cohesive exit strategy that utilizes every legal tool available to extract wealth while keeping your tax bill at an absolute minimum. You didn’t build a business to be “tax-rich” on paper and cash-poor in reality.

The 2026 tax landscape is more complex than ever. With federal personal tax brackets reaching 33% for income over $258,482, simply paying yourself a higher salary is a rookie mistake. You must balance your salary to cover your lifestyle and maximize your Individual Pension Plan (IPP) while using dividends to manage your personal tax exposure. It’s about precision. If you’re ready to stop guessing and start executing, book a tax optimization strategy session to review your current structure.

Maximizing the Capital Dividend Account (CDA)

The Capital Dividend Account is the holy grail of Canadian tax planning. It’s a notional account that tracks tax-free amounts your corporation can pay out to you. While most people only think of the non-taxable 50% of capital gains, the real power lies in life insurance. When your corporation receives a life insurance death benefit, the majority of that payout credits your CDA. This allows your heirs to pull millions out of the company completely tax-free. The CDA is the most powerful tax-free extraction tool for Canadians who are serious about building a multi-generational legacy.

The IPP: A High-Octane Alternative to the RRSP

If you’re over age 40 and earning a T4 income over $100,000, the RRSP is a toy. The 2026 RRSP contribution limit is capped at $33,810, which is barely enough to move the needle for a successful business owner. An Individual Pension Plan (IPP) allows for significantly higher contribution limits that grow as you age. Best of all? Your corporation can deduct 100% of these contributions as a business expense. You’re effectively shifting taxable corporate surplus into a protected retirement vehicle while reducing your current tax bill. It’s a breakthrough for anyone tired of the limitations of retail financial products.

- CDA Filing: Always file Form T2054 with the CRA before paying out dividends to avoid heavy penalties.

- CPP Optimization: With the 2026 YMPE at $74,600 and YAMPE at $85,000, your salary mix must account for maximum pensionable earnings.

- Deductibility: IPP administrative and actuarial fees are fully deductible for your corporation.

Executing Your Breakthrough: The Path to Financial Indestructibility

Knowledge isn’t power. Applied knowledge is power. Most business owners are “information junkies.” They read about corporate investment strategies canada but never pull the trigger. Why? Usually, it’s because they’re afraid of making a mistake. Or they’re too busy managing the day-to-day grind to actually lead their long-term wealth. You need a “Wake Up Call.” It’s time to stop being a passive observer of your own financial erosion. If you want to achieve a breakthrough, you have to move from contemplation to commitment.

Execution begins with a brutal audit of your current wealth leaks. Look at your 2025 and 2026 tax filings. How much did you lose to the “Passive Income Tax Trap”? If your passive income exceeded that $50,000 threshold, you likely triggered the 5:1 grind on your Small Business Deduction. These aren’t just numbers on a spreadsheet; they’re the holes in your bucket that prevent you from reaching peak performance. You cannot scale a legacy if you’re constantly bleeding capital to inefficient tax structures.

Once the leaks are identified, you restructure your corporate “vault” using the Financially Indestructible framework. This isn’t about buying a new product. It’s about changing your entire financial architecture. You shift your reserves from taxable accounts into specialized whole life structures where growth is contractually guaranteed and tax-free. You stop being a customer of the Big Five banks and start becoming your own source of liquidity. This is the only way to ensure your capital is ready for opportunity whenever it strikes.

Scaling with purpose means your money works as hard as you do. By integrating the advanced tools we’ve discussed, like the Capital Dividend Account and Individual Pension Plans, you ensure your impact lasts beyond your career. You’re building a fortress that protects your family for generations. This is how you win the game. You don’t just build a business; you build a financial engine that is truly indestructible.

The Financially Indestructible Coaching Program

Are you ready to stop being a “manager” and start being a “leader” of your wealth? Reading this guide is the first step, but real-world execution requires a seasoned mentor. My coaching program isn’t about abstract theory. It’s about personalized strategy sessions and one-on-one guidance designed to provoke immediate action. We don’t just talk about breakthroughs; we engineer them. Join the Wake Up Call to start your journey toward mastery today.

Your Next Move: Stop Overpaying and Start Growing

Don’t let another tax year bleed your corporation dry. Every day you wait is a day the CRA takes a piece of your legacy. The power of compound interest only works if you have a structure that prevents tax and volatility from resetting the clock. Take action now. Your future self will thank you for the tax-free freedom you build today. Sign up for the newsletter for weekly tactical sales and wealth insights that keep you on the cutting edge of corporate investment strategies canada.

Master Your Legacy: The Time for Strategy is Now

You’ve seen the brutal math of the 2026 tax landscape. Between the 38.67% federal tax on investment income and the aggressive SBD clawback, the system is rigged against the successful. But you didn’t build your business to act as a tax collector for the CRA. You’ve now learned how Corporate Infinite Banking and the Capital Dividend Account can transform your trapped surplus into a tax-efficient, liquid engine. Mastering corporate investment strategies canada isn’t about reading another guide; it’s about shifting your mindset and restructuring your wealth for impact.

Since 2012, I’ve provided direct, results-oriented coaching to entrepreneurs who refuse to settle for mediocrity. As the founder of the Financially Indestructible framework and an expert in Infinite Banking, I’m here to help you execute this breakthrough. You have the tools to build a fortress around your legacy. Don’t let another year of overpaying the CRA derail your progress. Book Your Financially Indestructible Strategy Session Today and take command of your capital. You’ve done the hard work of creating wealth; now let’s make sure you keep it. Your legacy is waiting.

Frequently Asked Questions

What is the best corporate investment strategy for small businesses in Canada?

The most effective corporate investment strategies canada focus on control and tax efficiency, specifically the Infinite Banking Concept. In 2026, with the federal investment tax rate at 38.67%, you can’t afford to leave capital in traditional taxable accounts. You need a structure that allows for growth and liquidity without triggering the CRA’s passive income trap. Stop chasing 1% yields and start building a private vault that protects your legacy.

How much passive income can a Canadian corporation earn before being taxed more?

A Canadian-controlled private corporation can earn up to $50,000 in passive investment income before the tax penalties kick in. Once you cross this threshold, the CRA reduces your $500,000 Small Business Deduction limit by $5 for every $1 of passive income. If your passive earnings hit $150,000, your SBD is wiped out entirely. This means your active business income will be taxed at the 15% general rate instead of the 9% small business rate.

Is corporate-owned life insurance a good investment in 2026?

Corporate-owned life insurance is an elite strategy in 2026 because it acts as a tax-free “And” asset. Unlike traditional investments subject to high corporate tax rates, the cash value in a participating whole life policy grows tax-exempt. It provides a contractually guaranteed return that doesn’t care about market volatility. It’s not just a death benefit; it’s a source of on-demand liquidity for your business operations.

Can I use my corporation to buy a car through Infinite Banking?

You absolutely can use your corporation to finance vehicles through Infinite Banking. Instead of paying interest to a Big Five bank, your corporation takes a policy loan against its insurance cash value to buy the car. You then “recapture” that wealth by paying the principal and interest back to your own company. This turns a depreciating expense into a process that builds your corporate asset base.

What is the difference between an IPP and an RRSP for business owners?

The primary difference is the contribution limit and tax deductibility. The 2026 RRSP limit is capped at $33,810, whereas an Individual Pension Plan (IPP) allows for significantly higher contributions that increase with age. 100% of IPP contributions and administrative fees are deductible for your corporation. For business owners over 40 earning more than $100,000, the IPP is the superior choice for high-octane wealth accumulation.

How do I get money out of my corporation tax-free in Canada?

The Capital Dividend Account (CDA) is your primary tool for tax-free extraction. This notional account allows you to pay out the non-taxable portion of capital gains and corporate-owned life insurance proceeds to shareholders without any personal tax hit. It’s the ultimate way to clear out trapped retained earnings. You must file Form T2054 with the CRA to authorize these payments and avoid penalties.

Does the CRA allow the Infinite Banking Concept?

The CRA permits this strategy because it’s built on the long-standing provisions of the Income Tax Act. Infinite Banking is a strategy, not a specific banking product, and it utilizes the tax-exempt status of life insurance policies. As long as your policy meets the “exempt test” defined by the CRA, your growth remains sheltered. It’s a legal, structural mastery of the existing tax code.

How does the Capital Dividend Account (CDA) actually work?

The CDA tracks specific tax-free amounts that can be distributed to Canadian residents. When your corporation realizes a capital gain, the 50% non-taxable portion is added to the CDA. Similarly, when a corporation receives a life insurance payout, the net amount is credited to the account. You can then issue a capital dividend to yourself, effectively pulling money out of the corporate structure with zero personal tax liability.