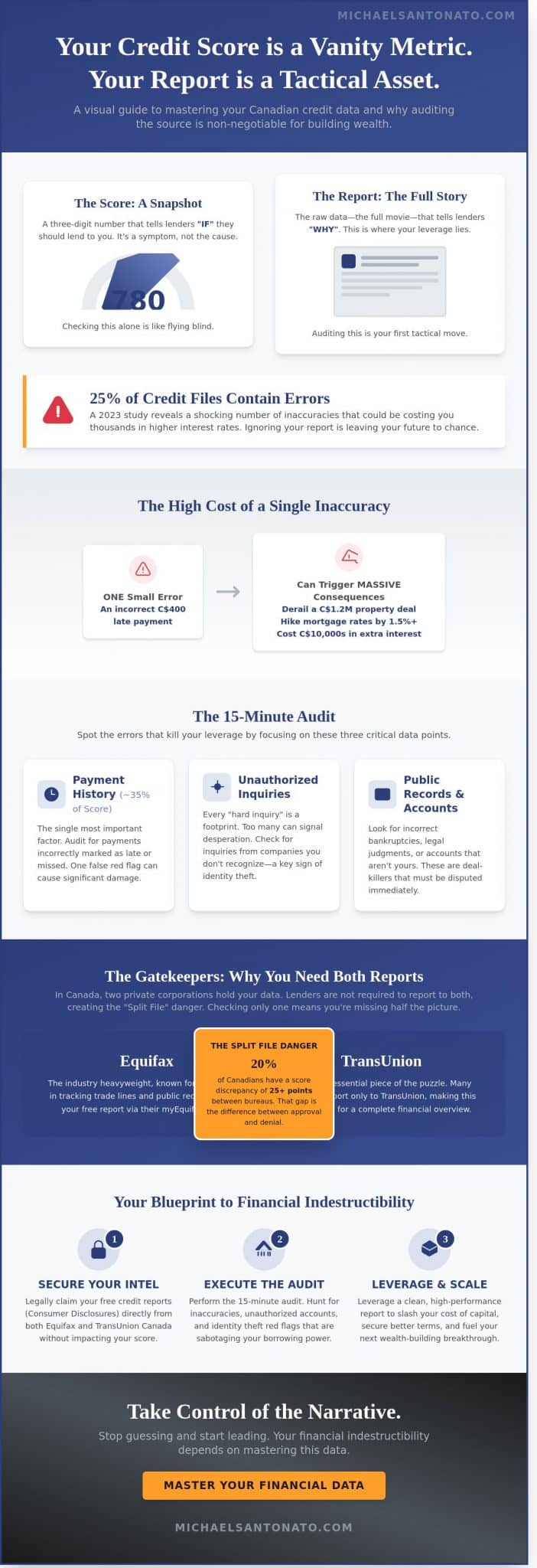

Are you mistaking a flashy app notification for real financial intelligence? Most Canadians check their credit score once a month and think they’re protected, yet a 2023 study found that roughly 25 percent of credit files contain errors that could spike your interest rates. Your score is a vanity metric, but your free credit report canada is the raw data that determines your financial legacy. If you aren’t auditing the actual source, you’re leaving your future to chance.

I understand the frustration of navigating complex bureau verification processes that feel designed to keep you in the dark. It’s time to stop guessing and start leading. This guide promises to hand you the blueprint for accessing your official Equifax and TransUnion reports without the typical headaches. We’ll break down how to spot identity theft red flags, fix damaging errors, and establish a foundation for total financial indestructibility. Get ready to master your data and scale your wealth with purpose.

Key Takeaways

- Stop flying blind and start treating your credit report as a high-stakes tactical asset rather than a vanity metric.

- Secure your free credit report canada from both major bureaus to ensure your financial intelligence is complete and accurate.

- Master the 15-minute audit to identify red flags and unauthorized accounts that are sabotaging your borrowing power.

- Leverage a clean, high-performance report to slash your cost of capital and fuel your next wealth-building breakthrough.

Stop Flying Blind: Why Your Free Credit Report is a Tactical Asset

Your financial reputation isn’t a suggestion. It’s a recorded fact. In Canada, your credit report serves as the ultimate dossier of your fiscal reliability. Most people treat their credit like a weather report; they check it, complain about it, and do nothing to change it. That stops now. If you want to build a legacy, you must stop playing defense. Accessing your free credit report canada is the first step in moving from a passive observer to a strategic commander of your capital. In 2026, the margin for error has vanished. Precision is the only way forward.

Ignorance is the most expensive tax you’ll ever pay. A single reporting error, such as an incorrectly flagged C$400 late payment from three years ago, can derail a C$1.2 million property investment. It can hike your mortgage interest rate by 1.5% or more, costing you tens of thousands of dollars over the term of the loan. You aren’t just looking for a number. You’re hunting for inaccuracies that threaten your ability to scale. This is about financial intelligence, not just checking a box.

The Difference Between a Score and a Report

Many Canadians obsess over their credit score while ignoring the report. This is a massive tactical error. Your score is a three-digit snapshot, but the report is the full-length movie. Understanding Your Credit Score requires looking at the raw data that feeds it. While the score tells a lender “if” they should lend to you, the report tells them “why.”

The report contains the critical data points that actually move the needle:

- Payment History: This accounts for roughly 35% of your total score. One missed window is a red flag.

- Hard Inquiries: Every time you chase credit, you leave a footprint that can signal desperation to a lender.

- Public Records: This is where bankruptcies or legal judgments hide, ready to sabotage your next big move.

A Consumer Disclosure is your legal right to see every single detail a bureau holds about your financial history without it impacting your score.

The “Financially Indestructible” Perspective on Credit

Elite performers don’t wait for a crisis to check their data. They audit their credit files quarterly to ensure they remain “financially indestructible.” This level of mastery is essential if you plan to implement high-level strategies like Infinite Banking Canada. You cannot become your own banker if your credit foundation is cracked. You need a pristine record to secure the best terms on the assets that will eventually fund your private banking system.

Credit mastery is the ultimate form of asset protection. By monitoring your free credit report canada frequently, you catch identity theft and clerical errors before they calcify into permanent damage. This isn’t about vanity; it’s about maintaining a weaponized financial profile that allows you to strike when opportunities arise in the 2026 market. Take control of the narrative before someone else writes it for you.

The Gatekeepers: Equifax vs. TransUnion in Canada

You wouldn’t enter a high-stakes negotiation with only half the facts. Why do it with your credit? In Canada, two titans hold the keys to your financial mobility: Equifax and TransUnion. They aren’t government agencies. They are private corporations that profit from your data. If you want to achieve financial mastery, you must understand how they operate. Stop guessing and start auditing.

Your data looks different on each bureau because lenders are not legally required to report to both. One bank might report your mortgage to Equifax, while your credit card provider only talks to TransUnion. This creates a “Split File” danger. If you only pull one free credit report canada offer, you are missing 50% of the picture. Industry data suggests that roughly 20% of Canadians have a discrepancy of 25 points or more between bureaus. That gap is the difference between an “Approved” and a “Denied” stamp on your next breakthrough deal.

Provincial laws, such as the Ontario Consumer Reporting Act and the Quebec Consumer Protection Act, guarantee your access. You have the legal right to see what these agencies say about you. Don’t let them hide behind paywalls or complex interfaces. Knowledge is your leverage.

Equifax Canada: The Industry Heavyweight

Equifax is the oldest player in the game. Their myEquifax portal provides a 30 day update cycle that tracks your trade lines with surgical precision. They prioritize public records, including bankruptcies and legal judgements. When you log in, they will bombard you with “Equifax Complete” upsells for C$19.95 or more per month. Ignore the noise. Look for the specific “Get your free credit report” link tucked away at the bottom of the dashboard. It is your right to access this data without a recurring subscription.

TransUnion Canada: The Essential Second Opinion

TransUnion uses different terminology. They call your detailed file a “Consumer Disclosure.” This is the document you need for a total audit. Many major Canadian lenders, including specific segments of the Big Five banks, prefer TransUnion’s data for auto loans and retail credit applications. Pay close attention to your employment history here. TransUnion often keeps more detailed records of your job titles and income declarations than its competitor. Verifying this ensures your financial foundation is built on solid ground, not outdated errors that could stall your growth.

- Check both bureaus: Errors often exist on one but not the other.

- Review monthly: Set a calendar reminder to catch identity theft early.

- Verify employment: Ensure your TransUnion file reflects your current professional status.

Step-by-Step: How to Claim Your Free Credit Report Today

Knowledge is power, but only if you act on it. You aren’t just looking at numbers; you’re auditing your financial legacy. To secure a free credit report canada offers, you have two primary paths. One is for the fast movers who want instant data. The other is for the meticulous record keepers who value a physical paper trail. Choose the one that fits your speed and get it done today. There is no excuse for remaining in the dark about your own data.

Option 1: The Instant Digital Download

Go straight to the source. Navigate to the official Equifax Canada and TransUnion Canada consumer portals. Avoid third-party sites that trade your data for marketing leads or trial subscriptions. Create your account using a secure, permanent email address. This is your command center. Once you’re in, download your PDF immediately. Digital hoarding is a smart strategy for your financial health. You need a baseline to track your breakthrough. Save every report in a secure folder to build a chronological history of your progress. This allows you to spot trends before they become problems.

Option 2: Mail and Phone Requests

Sometimes the digital path hits a wall. If you prefer a physical paper trail or if the online system glitches, go traditional. Call the Equifax automated line at 1-800-465-7166 or TransUnion at 1-800-663-9980 to access your free credit report canada provides through its regulated bureaus. Physical copies have a distinct advantage. They are often easier to mark up when you’re hunting for errors to dispute. You’ll need your Social Insurance Number and two pieces of valid identification ready. Expect a wait of 5 to 10 business days for the document to arrive in your mailbox. This isn’t a delay; it’s a commitment to total accuracy.

Handling Verification Failures

The system might tell you “Identity Not Verified.” Don’t panic. This isn’t a rejection; it’s a security protocol designed to protect your data from fraud. Knowledge-Based Authentication (KBA) questions often pull from data that’s 5 or 10 years old. If you have a thin credit file or recently moved, the algorithm might trip up. This is where most people quit. Don’t be most people. If the online portal fails, pick up the phone. Call the bureau directly to complete the verification. Mastery requires persistence. Your financial future is worth a 15 minute conversation to clear the air. If they require documentation, have your utility bills or passport scans ready to upload or mail immediately. Results don’t come to those who wait; they come to those who follow through.

The 15-Minute Audit: Spotting Errors That Kill Your Leverage

Your credit report isn’t a static document; it’s a living ledger of your financial reputation. Treat this audit like a high-stakes investigation. When you access your free credit report canada, look past the three-digit score. You’re hunting for inaccuracies that drain your borrowing power. Check every line for unauthorized inquiries. A single “hard hit” from a lender you never contacted can drop your score by 5 to 10 points instantly. Look for accounts you didn’t open. This isn’t just an error; it’s a breach of your financial perimeter. You need to be the primary guardian of your own data.

Identify “Zombie Debt.” In Canada, most negative information must be purged after six or seven years, depending on your province. If an old collection from 2018 is still haunting your 2026 report, it’s an illegal anchor on your progress. Even small errors in your address or employer history matter. Lenders use this data to verify stability. If your report shows five different addresses in three years because of typos, you look like a flight risk. Accuracy is the foundation of mastery. Correct these mistakes before they cost you a mortgage approval or a business loan.

Disputing Inaccuracies with Authority

Don’t just ask for a correction; demand it with hard evidence. Start by filing a formal dispute through Equifax or TransUnion Canada. Attach specific proof: bank statements, “paid in full” letters, or government ID. Under provincial consumer protection laws, bureaus generally have 30 to 60 days to investigate and respond. If they can’t verify the data, they must delete it. This is a tactical strike to reclaim your leverage. Be persistent. If the first response is a rejection, escalate to the provincial regulator to ensure your rights are respected.

Monitoring for Identity Mastery

Passive monitoring is for amateurs. High-performers practice active auditing. A “Credit Lock” is a decisive move to freeze your profile, preventing any new credit from being issued without your direct authorization. It’s the ultimate defensive play against identity theft. Watch for signs of dark web leaks, such as sudden “soft inquiries” from unknown sources or small “test” charges on dormant accounts. Your data is your legacy. Protect it with the same intensity you use to build your wealth. Real growth requires a secure foundation.

Stop letting errors dictate your financial ceiling. Take command of your financial future and master your wealth profile today.

Beyond Maintenance: Leveraging Your Credit for Wealth

Stop treating your credit score like a participation trophy. Checking a free credit report canada provides is the bare minimum. It is the baseline for entry. Real wealth starts when you stop playing defense and start using that data to scale a legacy. A clean report isn’t about avoiding debt; it’s about lowering the cost of capital for your next move. When your score sits above 760, you aren’t begging for a loan. You are negotiating terms. You are buying money at a discount to build a breakthrough. This shift in perspective is what separates the average consumer from the high-performer.

In the Financially Indestructible framework, credit is a pillar of strength, not a safety net. It allows you to move with speed. In a high-inflation environment, the ability to access C$100,000 or C$500,000 in liquidity at prime rates is a massive competitive advantage. If your report is cluttered with errors or late payments, you’re paying a “lazy tax” in the form of higher interest. Stop wasting resources. Clean the data, master the mechanics, and use your reputation to fund your future.

Credit as a Tool for Infinite Banking

To achieve total financial mastery, you must understand structural leverage. Your credit health directly dictates the efficiency of policy loans within an Infinite Banking strategy. Lenders look at your profile to determine the risk of your collateralized assets. High-performance credit can mean the difference of 2% to 3% in annual interest costs on third-party loans. That is pure profit staying in your pocket. Build a profile so robust that banks compete for your business. This requires disciplined data management and a commitment to excellence. You want to be the person lenders cannot say “no” to because your track record is flawless.

Your Next Breakthrough Starts Now

Analysis paralysis is the graveyard of ambition. You have the tools. You’ve accessed your free credit report canada. You know exactly where the cracks are. Now, will you use this information to build your fortress or let it sit on your hard drive? Most people wait for a “better time” to fix their finances. That time is a myth. Success belongs to those who take immediate, aggressive action.

You have the data. You have the strategy. The only variable left is your execution. If your wealth strategy feels too complex to handle alone, don’t guess. Seek professional coaching to bridge the gap between your current reality and the legacy you intend to leave. Your breakthrough is waiting on the other side of your next decision. Make it a bold one.

Take Command of Your Financial Legacy

Your financial future isn’t built on hope; it’s built on raw data and tactical execution. You’ve learned exactly how to claim your free credit report canada and why auditing Equifax and TransUnion files is the difference between stagnation and a massive breakthrough. Don’t let a single reporting error kill your leverage in 2026. Mastery requires you to treat your credit as a high-performance weapon for wealth, not just a defensive shield. Are you ready to stop playing small and start scaling with purpose?

As the founder of the Financially Indestructible framework, I’ve spent over a decade providing strategic financial coaching to Canadian professionals. I’m a specialist in the Infinite Banking Concept because I know that true impact comes from owning the system. You’ve got the tools to fix your score. Now, you need the elite strategy to turn that score into an impenetrable fortress. Let’s move beyond basic maintenance and start building your legacy today.

Ready to build a fortress around your wealth? Discover the Financially Indestructible Program.

The path to high performance is open. Take the lead and own your results.

Frequently Asked Questions

Does requesting my own free credit report lower my score in Canada?

No, checking your own credit report is a soft inquiry and has zero impact on your score. It’s a fundamental move for financial mastery. Hard inquiries happen when lenders check your file for new credit, but personal monitoring is 100% safe. Don’t let fear stop you from gaining intelligence. Take control of your data today.

How often can I get a free credit report from Equifax and TransUnion?

You can access your free credit report Canada online through Equifax and TransUnion as often as once a week in 2026. This frequency changed from the old once a year standard to help Canadians combat fraud. Use these weekly check-ins to build your financial legacy. Consistent monitoring ensures you spot errors before they sabotage your growth.

What is the difference between a credit report and a credit score?

Your credit report is the raw data of your financial history, while your score is a three digit summary of that performance. Think of the report as your full business transcript, and the score as your final grade. Scores in Canada typically range from 300 to 900. High achievers focus on the report details to ensure the score reflects their true impact.

Is it safe to provide my Social Insurance Number (SIN) to get my report?

Yes, providing your SIN is the most secure way to ensure the bureaus pull your specific file and not someone with a similar name. While it’s optional under Canadian law, it speeds up the verification process significantly. Protect your identity by only using official portals from Equifax, TransUnion, or verified partners. Mastery requires using the right tools safely.

How do I fix an error on my Canadian credit report?

You must file a formal dispute with Equifax or TransUnion using their specific investigation forms. Don’t wait for errors to vanish on their own. Attach your evidence, like bank statements or paid in full letters, to force a correction. The bureaus have 30 days to investigate under provincial consumer protection acts. Take decisive action to protect your financial reputation.

Why is my credit score different on different apps and websites?

Scores vary because providers use different proprietary algorithms, such as FICO Score 8 or VantageScore 3.0, to calculate your risk. One app might pull data from Equifax while another uses TransUnion. These bureaus don’t always share information instantly. Focus on the overall trend rather than minor 10 point fluctuations. Consistency in your habits is what creates a lasting breakthrough.

Can I get a free credit report if I am not a Canadian citizen?

Yes, any resident with a Canadian credit history can access their free credit report Canada regardless of citizenship status. You simply need a valid Canadian address and proper identification to verify your account. This includes international students and foreign workers on valid permits. Start building your Canadian legacy the moment you arrive by monitoring your file diligently.

What should I do if my request for a free credit report is denied?

First, verify that your identification details match your bank records exactly. Denials often stem from a thin file, meaning you haven’t used credit in Canada for at least 6 months. If your identity is confirmed but access is blocked, call the bureau’s consumer relations line immediately. Don’t accept a no when your financial future is on the line.