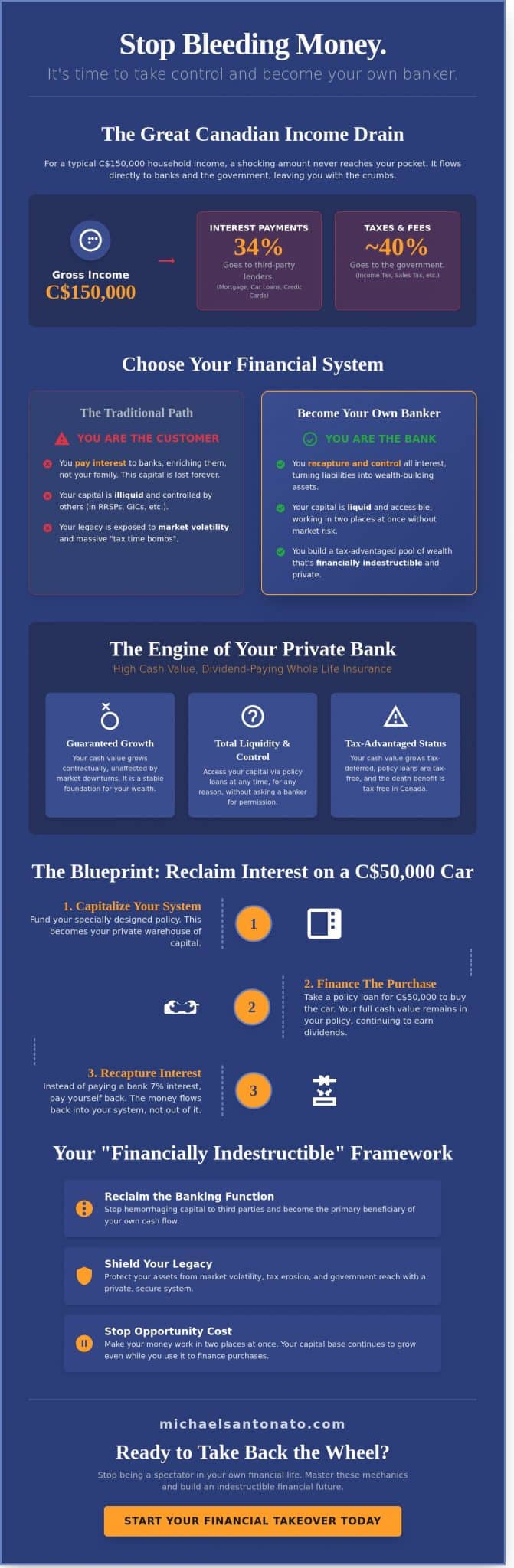

How much of your C$150,000 annual income is actually staying in your pocket after the Big Five banks and the CRA take their cut? Statistics show that the average Canadian family spends 34% of their gross income on interest payments alone. You’re grinding for the bank, not for your own future. It’s time to stop being a spectator in your financial life. Becoming your own banker isn’t just a strategy; it’s a hostile takeover of your own cash flow. You deserve to keep the profit that the banks have been stealing from your hard work for decades.

You already know the system is designed to keep your capital illiquid and under someone else’s control. You’re tired of watching tax erosion eat your legacy before it even has a chance to grow. This guide will show you exactly how to reclaim the banking function, eliminate third-party interest, and build a pool of wealth that’s completely indestructible. We’re breaking down the mechanics of self-financing and the exact steps you need to take to achieve total financial mastery by 2026. Get ready to shift your mindset and take back the wheel.

Key Takeaways

- Stop hemorrhaging capital to third-party lenders and reclaim the banking function as the most powerful driver of your personal economy.

- Discover why high cash value dividend-paying life insurance is the only non-negotiable engine for building liquid, tax-advantaged wealth in Canada.

- Master the step-by-step blueprint for becoming your own banker to recapture interest on major C$ purchases and turn liabilities into wealth-building assets.

- Expose the “tax time bombs” hidden in traditional investment advice and learn how to shield your legacy from market volatility and government reach.

- Integrate these high-performance strategies into a “Financially Indestructible” framework designed to protect your assets and scale your impact for generations.

The Paradigm Shift: What It Really Means to Become Your Own Banker

Most Canadians think banking is a physical building representing a traditional financial institution. They are wrong. Banking is not a place; it is a process. In fact, it is the most vital process in any economy. Right now, you are likely on the wrong side of that process. You work 40 hours a week, yet a massive chunk of your labor flows directly to third-party lenders through interest and fees. It is time to stop being the bank’s best customer and start becoming your own banker.

When you finance a purchase through a traditional lender, you pay them for the privilege of using their capital. When you pay cash, you give up the ability to earn interest on that money forever. This is the hidden killer of wealth known as Opportunity Cost. Every C$1.00 you spend is actually worth much more over time. If you do not control the banking function in your life, someone else will. They will profit from your need for capital while you settle for the crumbs. You must view your finances as a private, closed-loop system where you are the primary beneficiary of every transaction.

The Nelson Nash Legacy and the IBC Foundation

This strategy is not a “get rich quick” scheme. It is a disciplined methodology pioneered by R. Nelson Nash, the visionary who authored the Infinite Banking Concept (IBC). In 2026, with Canadian household debt sitting near 180% of disposable income, these principles are more relevant than ever. Traditional banking relies on you staying in a cycle of perpetual debt. Privatized banking, however, focuses on building a warehouse of wealth that you control. It is the difference between being a tenant in the financial system and being the landlord of your own legacy.

Why Your Current Financial Strategy is Leaking Wealth

Your wealth is leaking through a thousand small cuts. Think about your last car loan or your current mortgage. Who is actually getting rich off your hard work? It is not you. It is the car company’s finance arm and the big five banks. When you pay interest to an outside source, that money is gone from your family’s reach forever. This interest drain is a massive barrier to achieving high-level performance in your personal economy.

To stop the bleed, you must adopt a “Financially Indestructible” mindset. This means reclaiming every dollar that would otherwise leave your circle. Consider these points:

- The average Canadian pays thousands in interest over their lifetime on depreciating assets.

- Traditional savings accounts in Canada often offer returns that fail to keep pace with inflation.

- By becoming your own banker, you capture the interest that used to go to strangers.

Stop settling for mediocre results. You can start mastering these mechanics today by visiting truefinancialeducation.com. It is time to shift your perspective, plug the leaks, and scale your wealth with purpose.

The Engine of Mastery: Why Dividend-Paying Whole Life Insurance is Non-Negotiable

Stop looking at life insurance as a death benefit. If you want to succeed at becoming your own banker, you need a high cash value policy designed for liquidity, not just a payout when you’re gone. Most people buy insurance for the wrong reasons. They want the cheapest monthly cost, so they buy Term. That’s like renting a home and hoping the landlord never kicks you out. Or they buy Universal Life, where the costs of insurance can skyrocket as they age, eating their savings alive. Those products are designed for the insurance company’s bottom line, not yours.

You need a specific type of dividend-paying whole life insurance from a mutual company. This isn’t an investment. It’s the warehouse where your C$ capital lives. Think of it as a private vault that allows your money to work in two places at once. When you understand this, you stop chasing 8 percent returns in volatile markets and start focusing on the efficiency of your capital. You’re building a system where you control the flow of every C$1 you earn. This requires a professional who understands the specific engineering of an “Infinite Banking” structure; otherwise, you’re just buying a standard policy that won’t have the liquidity you need in the early years.

Cash Value vs. Death Benefit: The Liquidity Secret

The magic happens in the cash value. This is your accessible capital. In Canada, this growth is tax-deferred under the Income Tax Act, meaning your wealth compounds without the government taking a cut every year. The real power lies in the “unstructured loan” feature. You don’t ask a bank for permission to use your money. You tell the insurance company you’re taking a loan against your cash value. They don’t ask for a credit check or a business plan. You stay in total control of the repayment terms. Many savvy Canadians are already Using Infinite Banking For Passive Multifamily Investing to create multiple streams of income while their original capital continues to grow inside the policy. Guaranteed growth is the bedrock of financial peace.

The Power of Dividends and Mutual Companies

You must work with a mutual insurance company. Why? Because in a mutual structure, you’re a part-owner. You aren’t just a policyholder; you’re a stakeholder. When the company profited in 2023, those profits were distributed to policyholders as dividends. These dividends are technically a “return of premium,” which makes them incredibly tax-efficient in the Canadian market. They act as the turbocharger for your banking engine, increasing both your cash value and your death benefit over time. To truly master these mechanics, you can dive into the technical details at True Financial Education. Don’t settle for a mediocre financial setup when you can build a legacy. If you’re ready to stop being a slave to traditional lenders, it’s time to start building your own private reserve today.

Debunking the Critics: Why Traditional Advice is Keeping You Broke

You have heard the noise. The “Bogleheads” and the “Buy Term, Invest the Difference” crowd want you to play it safe. They tell you to dump your hard-earned C$ into a volatile market and wait 40 years. That isn’t a strategy. It’s a prayer. These critics ignore the brutal reality of market volatility. If your portfolio drops 50% one year and gains 50% the next, your “average” return is 0%. Your actual account balance, however, is down 25%. That is a mathematical lie that keeps families broke. When you focus on Infinite Banking – Becoming Your Own Banker, you trade that market hope for mathematical certainty. The process of becoming your own banker requires you to stop thinking like a consumer and start thinking like a bank owner. You need mastery over your cash flow, not a 40-year hope that the TSX behaves itself.

The Myth of the RRSP

The Canadian RRSP is often sold as a “tax break.” I call it a tax time bomb. You’re deferring taxes today at a known rate to pay them later at an unknown, likely higher rate. You’re also locking your capital in a government-regulated cage. Try accessing that money before age 65 without a penalty or a massive tax hit. It’s fragile. Government-sponsored plans are subject to the whims of shifting legislation. In contrast, a properly structured IBC policy is an indestructible private contract. You own it. You control the flow. You don’t need permission from the CRA to use your own capital for a breakthrough business opportunity or a major purchase.

Addressing the ‘Fees’ Argument Head-On

Critics love to point at the front-loaded costs of a dividend-paying whole life policy. They’re right. It’s expensive to build a bank. Do you think starting a Royal Bank or TD branch is free? You aren’t buying a “product.” You’re building a multi-generational financial system. The “low fees” in a mutual fund or ETF don’t protect you from a 30% market crash. They don’t provide a death benefit. They don’t offer guaranteed liquidity. In a properly structured policy, those initial costs are the price of admission for a lifetime of tax-free growth and access. By year 10 or 12, the annual growth often outpaces every dollar you put in. That is how you scale with purpose and leave a legacy. Stop tripping over pennies while you lose dollars to the banks and the taxman.

The Implementation Blueprint: Reclaiming Interest on Major Purchases

You’ve understood the theory. Now it’s time for execution. Most people spend their lives making everyone else rich. They pay interest to banks, finance companies, and credit card issuers. When you commit to becoming your own banker, you flip the script. You stop the leak. You keep the interest that used to leave your household. This isn’t just about saving; it’s about recapturing the volume of interest you lose every single day. You need to treat your capital with the same respect a bank does.

Success requires a disciplined five-step process:

- Step 1: Capitalize your system. This is the seed phase. You fund your high cash value life insurance policy. You’re building the reservoir. Without capital, there’s no bank.

- Step 2: Identify a purchase. Think about a C$50,000 vehicle or a major renovation. You were already going to make this purchase.

- Step 3: Take a policy loan. Use your cash value as collateral. The insurance company provides the funds. You pay cash for the item, putting you in a position of power.

- Step 4: Pay yourself back with interest. This is the Reclamation phase. You set a repayment schedule at least equal to what a commercial lender would charge.

- Step 5: Repeat and scale. Once the loan is recovered, the system is ready for the next move. You apply this across every area of your life.

Case Study: Financing Your Next Vehicle

Look at the math. A standard C$50,000 car loan at 8% over five years costs you roughly C$10,800 in interest. That money is gone forever. With the IBC method, your C$50,000 in cash value stays in the policy. It never stops compounding. You take a loan against it, pay the dealer, and then pay your policy back. By the end of five years, you own the car, the loan is gone, and your original C$50,000 has grown significantly because it never left the account. This strategy is a cornerstone of Infinite Banking Canada: The 2026 Guide. You’re not just buying a car; you’re building a legacy.

Business Owners: Using Your Bank for Cash Flow

Entrepreneurs use this to achieve a breakthrough in scaling. Why beg a bank for an operating line? Use your policy to fund inventory or C$100,000 in tax payments. This “double-play” allows your capital to grow inside the policy while it simultaneously works for your business growth. This is the reality of becoming your own banker as a business owner. You gain total control over your cash flow. You stop being a slave to external lending cycles. It is the ultimate tool for high-performance growth and scaling with purpose.

Ready to take control of your financial destiny? Book your strategy session and start building your bank today.

Building Your Legacy: Integrating BYOB into a Financially Indestructible Framework

Becoming your own banker is a massive first step, but it isn’t the finish line. It’s one pillar in a larger, Financially Indestructible framework designed to shield your wealth from the three biggest threats: taxes, market volatility, and litigation. In the Canadian context, where the top marginal tax rate can exceed 53.5% in provinces like Ontario or Quebec, simply “saving” isn’t enough. You need a fortress. You need a system that ensures your capital is protected and accessible when opportunities arise.

Mastery of this system doesn’t happen by accident. You can read the book ten times and still fail if you don’t execute with precision. This is about moving from theory to impactful action. You need tax-free wealth planning that integrates with Canadian corporate structures and personal estate laws. Most people play defense. We play offense. We build systems where every dollar does three jobs at once. That requires a coach, not just a manual. A book can’t hold you accountable when you’re tempted to skip a premium or mismanage a loan repayment.

Scaling with Purpose and Discipline

Don’t stop at a single policy. The true power of becoming your own banker reveals itself when you scale. This means expanding the system to cover your spouse, your children, and even your business partners. You’re building a “Family Bank” that survives for generations. Imagine your grandchildren financing their first homes or business ventures through a family-controlled pool of capital rather than a big five bank. This isn’t just about money; it’s about control. Private wealth coaching ensures you maintain the discipline to expand the system. Without that accountability, most systems collapse under the weight of human nature.

Your Next Step Toward Financial Breakthrough

Stop being a spectator in your own financial life. The difference between those who build legacies and those who just get by is the willingness to take decisive action. A strategy session with Michael Santonato isn’t a casual chat. It’s a deep dive into your current numbers, your tax liabilities, and your 10-year vision. We identify the leaks in your current bucket and plug them with a customized, indestructible plan. You’ll walk away with a roadmap, not a list of suggestions. The time for “thinking about it” is over. It’s time for a breakthrough. Apply for the Financially Indestructible Program Today and start taking control of your future.

Stop Funding the Banks and Start Funding Your Legacy

Traditional financial advice is designed to keep you broke while the big banks thrive on your interest payments. It’s time to stop surrendering your hard-earned capital. By becoming your own banker, you reclaim the interest on every major purchase and turn your expenses into a growing pool of wealth. This shift requires a non-negotiable engine: dividend-paying whole life insurance. This isn’t a theory; it’s a proven blueprint for building a financially indestructible future that protects your family for generations.

Michael Santonato brings over a decade of high-performance coaching to the table. As an expert in the Financially Indestructible framework and a specialist in Canadian IBC implementation, he knows how to navigate the unique regulations of the Canadian market. You’ve seen the mechanics of mastery. Now, you need the strategy to execute without error. Stop waiting for the economy to change and start changing your own economy today.

Take Control of Your Legacy: Book Your Private Strategy Session with Michael Santonato

Your journey to absolute financial sovereignty starts with a single, decisive action. You’ve got the tools, so let’s build something that lasts.

Frequently Asked Questions

Is Becoming Your Own Banker the same as the Infinite Banking Concept?

Yes, they’re identical in practice. Nelson Nash released his seminal book in 2000 titled “Becoming Your Own Banker” to introduce the Infinite Banking Concept to the world. It’s a strategy, not a specific product. You’re using a financial vehicle to take control of the banking function in your life. Stop overcomplicating the terminology. It’s simply about shifting who keeps the interest on the money you’re already spending.

Can I use any whole life insurance policy to become my own banker?

No, standard off-the-shelf policies won’t work. To succeed at becoming your own banker, you need a high cash value, dividend-paying participating whole life policy from a mutual insurance company. Most policies are designed for death benefits only. Yours must be engineered for maximum early cash accumulation. If it’s not structured correctly from day one, the strategy fails. Demand a policy that prioritizes your liquidity over the agent’s commission.

How long does it take before I can start borrowing from my policy?

You can typically access funds within 30 to 90 days of your first premium payment. Most Canadian mutual companies allow you to leverage your cash value almost immediately once the policy is in force. Don’t wait for years to see results. You want your capital working for you now. The speed of your liquidity depends entirely on how your specialist designs the contract and how much you contribute upfront.

What happens if I don’t pay back the loan to my own bank?

Your death benefit decreases by the outstanding loan amount plus accrued interest. There’s no “loan police” coming after you; you’re the banker. However, failing to repay ruins the compounding effect of your system. You’re stealing from your future self. Treat your policy with more respect than you’d treat a traditional lender if you want to build a real legacy. Pay yourself back with interest to grow your pool faster.

Is this strategy legal in both Canada and the United States?

Yes, it’s fully legal and regulated in both countries. In Canada, these policies must comply with Section 148 of the Income Tax Act to maintain their tax-exempt status. While the core principles remain the same, the tax codes differ between the CRA and the IRS. Ensure your plan is built by a Canadian specialist who understands our specific 2017 tax rule changes. Don’t use American templates for Canadian wealth.

Do I still need to have a traditional bank account if I do this?

Yes, you’ll still use a traditional bank for your daily “triage” of cash. Think of the big banks as a clearinghouse for your monthly bills and the policy as your private vault. You don’t need them for financing major purchases anymore, but you still need a place for direct deposits and e-transfers. Move money through the bank, not to it. Use their infrastructure without giving them your profit.

Is the death benefit taxable when it passes to my heirs?

No, death benefits are paid out tax-free to your beneficiaries in Canada. This is one of the last great tax advantages available under Canadian law. Your heirs receive the full amount without the CRA taking a 25 percent or 50 percent cut like they would with an RRSP or RRIF. It’s the ultimate tool for passing down a clean, liquid legacy. Protect your family from the taxman’s reach through proactive planning.

How does ‘Becoming Your Own Banker’ help with my taxes?

Becoming your own banker allows your wealth to grow on a tax-deferred basis inside the policy. You can access that capital through policy loans without triggering a taxable event. This creates a pool of tax-free liquidity you can use for investments or business growth. It’s about maximizing efficiency. Why pay 53 percent tax on interest income when you can grow it sheltered? Stop handing your hard-earned gains to the government.