How Much Did CPP and OAS Increase in 2025? The Canadian Retirement Reality Check

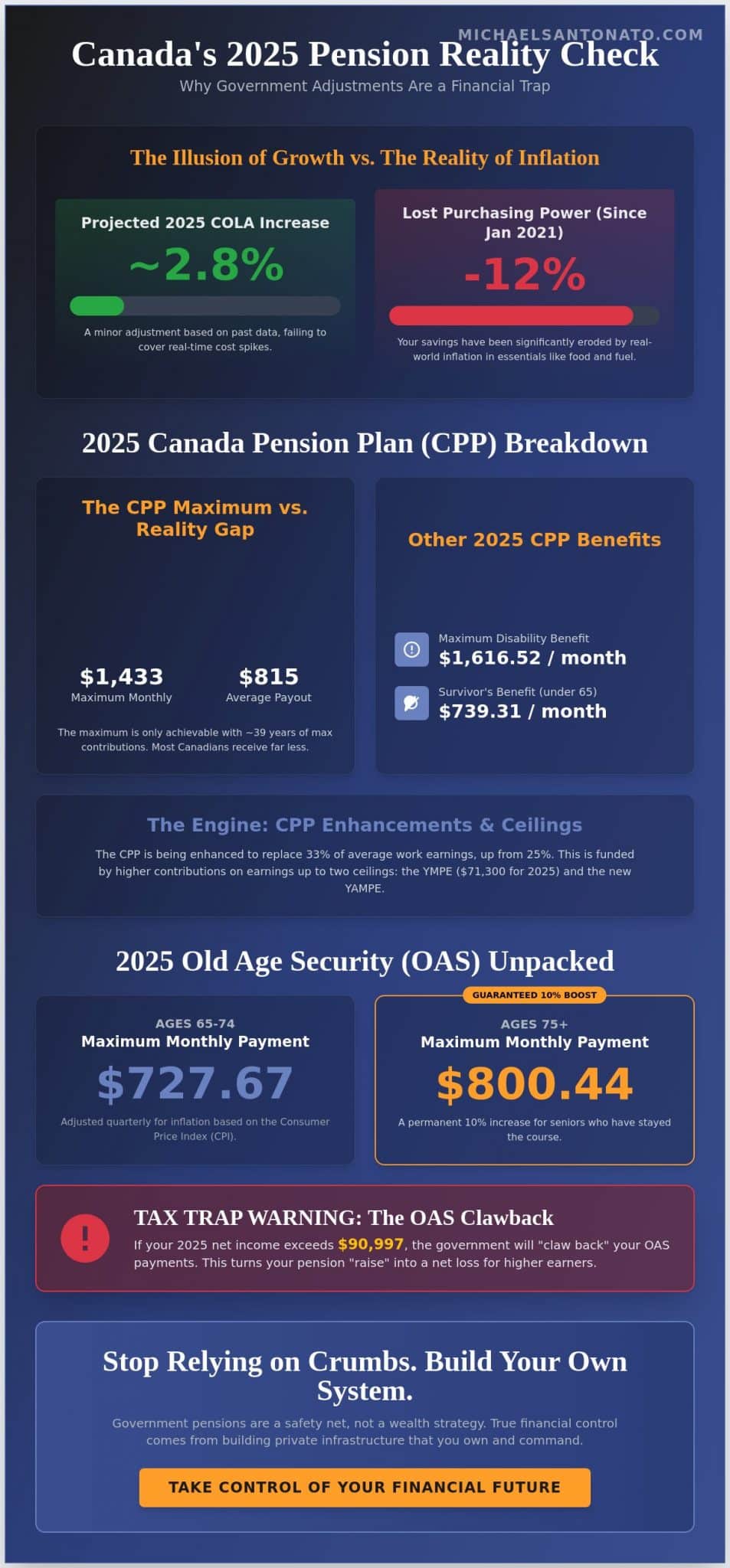

Are you really going to bet your entire legacy on a government cost-of-living adjustment that barely covers a week of groceries? If you are waiting to find out how much will cpp and oas increase in 2025 canada to see if you can finally afford to breathe, you have already lost the game. While the 2025 increase is projected to sit near 2.8 percent, inflation has stripped over 12 percent of purchasing power from seniors since January 2021. Relying on these crumbs isn’t a retirement plan; it’s a slow-motion financial disaster that leaves your future in the hands of bureaucrats.

I know you feel the weight of every dollar being eroded by a system that takes more than it gives. It’s frustrating to watch your hard-earned CPP enhancements get swallowed by higher payroll taxes before you even see a dime. I’m going to give you the exact 2025 payment figures so you have the facts, but I’m also going to expose why these increases are a trap that triggers the dreaded OAS clawback for anyone earning over $90,997. You’ll learn how to pivot from government dependency to a private wealth structure that is truly indestructible. We are breaking down the 2025 benefit reality and building your strategy for total financial mastery.

Key Takeaways

- Get the hard facts on how much will cpp and oas increase in 2025 canada and why the new C$1,433 monthly maximum is still a trap for the unprepared.

- Discover why the 2.6% cost-of-living adjustment is “yesterday’s news” and fails to protect your purchasing power against double-digit spikes in food and fuel.

- Master the 2025 OAS clawback thresholds to ensure your government “raise” doesn’t accidentally trigger a tax trap that slashes your net income.

- Break free from pension uncertainty by building private financial infrastructure that puts you in total control of the banking function in your own life.

- Shift your mindset from waiting for government crumbs to creating an indestructible retirement legacy through the Infinite Banking Concept.

The 2025 CPP and OAS Numbers: What Actually Changed?

Stop guessing about your future. The 2025 numbers are live, and they demand your attention. A 2.6% increase might sound like a minor adjustment, but in the world of high performance wealth building, every decimal point counts. This cost of living adjustment is the government’s attempt to keep pace with the inflation that’s been eating your purchasing power. If you are asking how much will cpp and oas increase in 2025 canada, you need to look at the hard data. You are looking at a fundamental shift in Canada’s public retirement income system that rewards those who have mastered their career earnings.

For new retirees hitting age 65 in 2025, the maximum CPP monthly benefit has jumped to C$1,433.00. That is a concrete benchmark for your planning. But let’s be real; most Canadians won’t see that maximum because they didn’t contribute enough over their working life. Are you playing for pennies, or are you building a legacy? Understanding these ceilings is the first step toward financial mastery. You can find more resources on building this foundation at truefinancialeducation.com.

CPP Maximums and the Enhancement Impact

The 2025 YMPE is $71,300 to establish technical authority. This is the first ceiling you need to clear. Above that, we now have the Year’s Additional Maximum Pensionable Earnings (YAMPE). This “Second Ceiling” is part of a multi year breakthrough designed to move income replacement from 25% to 33%. For your 2026 bottom line, this means higher contributions now for a significantly larger payout later. It’s about scaling your future with purpose. Don’t overlook the secondary benefits either. The maximum monthly disability benefit for 2025 has climbed to C$1,616.52, while survivor benefits for those under 65 sit at C$739.31. These numbers represent the pragmatism required to protect your family’s impact.

OAS Increases: The Age 75 Bonus

Old Age Security operates on a different rhythm. It adjusts quarterly based on the Consumer Price Index, ensuring your benefits don’t stagnate. For the start of 2025, seniors aged 65 to 74 can expect a maximum monthly payment of C$727.67. If you’ve reached age 75, that 10% permanent increase kicks in. This brings the maximum for the 75 plus bracket to C$800.44 per month. This isn’t a suggestion; it’s a guaranteed boost for those who have stayed the course. To claim the full amount, you must meet the 40 year residency requirement after age 18. If you haven’t put in the time, your check will be prorated. The math is simple, and the results are final. Do you have a strategy to bridge the gap if your OAS falls short?

Decoding the Mechanism: How Canada Calculates Your ‘Raise’

Stop waiting for a handout. The “raise” you’re expecting in your CPP and OAS isn’t a bonus or a reward for your service. It’s a reaction. The federal government isn’t looking at your current grocery bill when they cut your check. They’re looking at the rearview mirror. When you ask how much will cpp and oas increase in 2025 canada, you’re looking at a percentage that’s already behind the curve. You’re playing a game of catch-up where the rules are written by yesterday’s data.

The CPI and Inflation Indexing

The government uses the Consumer Price Index (CPI) to measure a “basket of goods.” This includes food, shelter, and transportation. But here’s the reality check: your personal inflation rate is likely much higher than the official number. OAS payments adjust every quarter in January, April, July, and October. CPP only adjusts once a year in January. This annual lag means your 2025 purchasing power is being dictated by 2024 inflation. If prices spike in February, you’re stuck waiting until the next year for a correction. It’s a slow-motion response to a fast-moving problem.

The Reality of the ‘Average’ Payment

Don’t get blinded by the “Maximum Benefit” headlines. That’s a trap for the unprepared. To hit the maximum CPP, you must contribute at the ceiling for at least 39 years. Most Canadians don’t come close. In July 2024, the average new CPP recipient took home just C$815.00 per month. That’s a massive gap from the C$1,364.60 maximum. Years of low earnings or career breaks for family care slash your legacy. You need to stop guessing and get the raw data. Log into your My Service Canada Account to see your actual projected numbers. If those numbers don’t support your vision, it’s time for a breakthrough in your strategy. You can start building that financial mastery right now.

Understanding how much will cpp and oas increase in 2025 canada is only half the battle. The real mastery comes from knowing how to bridge the gap between what the government gives and what you actually need to thrive. Relying on a system that uses lagging data is a recipe for mediocrity. You’ve worked too hard to settle for an “average” retirement. Take control of the variables you can influence and stop leaving your future to a federal calculation.

The Inflation Trap: Why a 2.6% Increase Is Not a Win

Are you really celebrating a 2.6% raise when your grocery bill and fuel costs have spiked by double digits? Let’s get real. If you’re asking how much will cpp and oas increase in 2025 canada, you’re looking at the wrong metrics. A 2.6% bump is a participation trophy from the government. It’s designed to keep you afloat, not to help you thrive. While the official Consumer Price Index claims inflation is stabilizing, your bank account tells a different story. Food prices in Canada rose nearly 23% between 2021 and 2024. A tiny adjustment in your pension doesn’t cover that gap. It barely scratches the surface of your lost purchasing power.

Think about what your money actually does. In 2020, a maximum monthly CPP payment of roughly C$1,175 could cover a significant portion of basic living expenses in many Canadian cities. By 2025, even with the projected increase bringing that maximum closer to C$1,433, that money vanishes instantly. Rent, utilities, and insurance have outpaced these adjustments by a mile. You can’t save your way out of a currency that’s being devalued by the day. You need assets that grow faster than the government can print money. Relying on a 2.6% increase to maintain your lifestyle is a recipe for a mediocre retirement.

The Silent Thief of Retirement

Real Yield is the only number that matters for your legacy. If your pension goes up 2.6% but your actual cost of living increases by 5%, your Real Yield is negative 2.4%. You’re getting poorer, just at a slower pace. In the Financially Indestructible framework, government-indexed income is a floor, never a ceiling. Stop being a pension passenger. Stop waiting for a bureaucrat in Ottawa to decide your quality of life. You’re a high-performer. Take the wheel and build a breakthrough strategy that doesn’t rely on government crumbs.

Breaking the Dependency Cycle

The “guaranteed” check is an emotional trap. It creates a false sense of security that kills ambition and stops you from seeking true financial mastery. High-performers need a strategy that doesn’t have a government-imposed ceiling. Why should your lifestyle be limited by a federal formula? You need to become your own source of liquidity and growth. To see how elite Canadians are building wealth that the taxman can’t touch and inflation can’t erode, explore Infinite Banking Canada: The 2026 Guide to Financial Indestructibility. Don’t let a 2.6% increase be the highlight of your year. Aim for an impact that lasts generations.

OAS Clawbacks and Tax Traps: Protecting Your Income

Success has a price in Canada; it’s called the OAS recovery tax. If your net world income exceeds $90,997 for the 2024 tax year, the CRA begins clawing back your Old Age Security payments starting in July 2025. This 15% recovery tax isn’t just a fee; it’s a direct penalty on your disciplined saving. You worked for decades to build your nest egg, but without a tactical plan, the government becomes your most expensive partner. When you look at how much will cpp and oas increase in 2025 canada, you must also calculate how much of that increase you actually keep.

The math is often a trap. A “raise” in your CPP benefits can actually trigger a “cut” in your OAS. If the 2025 CPP enhancement pushes your total income over the $90,997 threshold, your OAS payment drops by 15 cents for every extra dollar earned. You’re running on a treadmill just to stay in the same place. Every dollar of pension income is a target for the CRA. You need to achieve tax mastery to stop this leakage. One powerful move is strategic deferral. Waiting until age 70 can increase your OAS by 36% and your CPP by 42%. It’s a breakthrough for your long-term legacy, but only if you have the liquid cash flow to bridge the gap until then.

Navigating the Recovery Tax Threshold

High-income retirees are penalized for their success. To protect your income, you must lower your taxable net income without starving your lifestyle. Use your TFSA as an “invisible” income source. Withdrawals from a TFSA don’t count toward the $90,997 limit. This is a tactical advantage that preserves your OAS eligibility. Shift your focus from total wealth to after-tax impact. If you don’t manage your tax brackets, you’re essentially acting as a collection agent for the government.

Tax Optimization for the Modern Retiree

Your RRSP is a tax time bomb. Mandatory RRIF withdrawals at age 72 often collide with your CPP and OAS, exploding your taxable income and triggering massive clawbacks. Use pension income splitting with your spouse to keep both of you under the clawback limits. This balances the tax load and preserves your benefits. For elite strategies on tax filing and optimization, visit True Financial Education to ensure you aren’t leaving money on the table. Understanding how much will cpp and oas increase in 2025 canada is only half the battle; keeping that money is where you win.

Don’t let the CRA dictate your retirement legacy. Book a breakthrough session with Michael Santonato to secure your cash flow today.

Beyond the Crumb-Picking: Building Private Infrastructure

Stop waiting for a miracle from Ottawa. Most Canadians spend their energy wondering how much will cpp and oas increase in 2025 canada, hoping for a few extra dollars to offset the rising cost of groceries. That is a survivalist mindset. If you want true freedom, you need to stop picking up crumbs and start building your own private infrastructure. You need to become Financially Indestructible. This means taking over the banking function in your life so you aren’t at the mercy of federal budget votes or shifting political winds.

When you rely on government programs, your lifestyle is subject to a committee decision. When you own the system, you set the rules. This is about moving from a position of dependency to a position of absolute power. You don’t build a legacy on indexed inflation adjustments. You build it on assets you control.

The Infinite Banking Advantage

The Infinite Banking Concept (IBC) is the ultimate hedge against pension uncertainty. By using dividend-paying whole life insurance, you create a private, tax-free pool of capital that functions as your own pension fund. Consider the difference between a government promise and a private guarantee. The CPP is a massive, slow-moving ship vulnerable to demographic shifts and economic downturns. In contrast, a properly structured policy provides contractual guarantees for cash value growth and a death benefit.

- Liquidity: Access your capital without begging a loan officer or justifying your purchase.

- Control: You decide how and when to use your wealth, not a government bureaucrat.

- Tax Efficiency: Grow your legacy without the tax man taking a massive cut of your gains.

The 2025 CPP increases are mathematically insignificant for anyone serious about high-level performance. Why settle for a minor cost-of-living adjustment when you can own the bank? When you capitalize your own system, you stop being a spectator in your own financial life.

Mastering Your Financial Legacy

You must shift from a consumer mindset to a capitalist mindset. Consumers worry about monthly checks. Capitalists focus on asset control and cash flow velocity. Building a legacy that lasts for generations requires a strategy that doesn’t expire when you do. To move toward a Financially Indestructible state, follow this 3-step audit today:

- Calculate your Gap: Compare your projected government benefits against the actual cost of the lifestyle you demand.

- Identify Leakage: Find exactly where your interest and tax dollars are escaping to external institutions.

- Recapture the Flow: Redirect those dollars into your own private banking system to build equity.

Your retirement shouldn’t be a reality check of what you have to give up. It should be a breakthrough into what you can achieve. Stop playing small. It’s time to move beyond government dependency and take full ownership of your future. If you are ready to stop asking how much will cpp and oas increase in 2025 canada and start asking how much you can grow your own bank, let’s talk.

Take the first step toward mastery. Book a strategy session today and start building your private infrastructure. Don’t leave your legacy to chance.

Take Command of Your Financial Legacy Today

You now know exactly how much will cpp and oas increase in 2025 canada, but understanding the numbers is only half the battle. A 2.6 percent adjustment is a drop in the bucket when real-world inflation is gutting your purchasing power every single day. Don’t let government crumbs and OAS clawbacks dictate your quality of life. You’ve spent decades building your career; it’s time to protect what’s yours with a private infrastructure that the CRA can’t touch. My proven framework for tax-free wealth planning is built on over 12 years of financial coaching expertise. As a specialist in the Infinite Banking Concept in Canada, I help high-achievers move beyond survival mode into true financial mastery. Stop waiting for a policy change to save your retirement. You have the power to create a breakthrough right now. Ready to stop relying on government crumbs? Join the Financially Indestructible Program today. You’re closer to financial freedom than you think, and the path starts with a single decisive move.

Frequently Asked Questions

What is the maximum CPP payment for 2025?

The maximum monthly CPP payment for a new beneficiary starting at age 65 in 2025 is C$1,364.60. This figure is tied to the Year’s Maximum Pensionable Earnings, which the government set at C$71,300 for the 2025 calendar year. Don’t settle for the average payment of roughly C$831; you need to understand your contribution history to hit these peak numbers. Mastery of your retirement cash flow starts with knowing these hard limits.

How much did OAS increase for seniors over 75 in 2025?

Seniors aged 75 and older receive a permanent 10 percent increase to their Old Age Security pension compared to those under 75. For the first quarter of 2025, the maximum monthly amount for this age group is C$790.16. This extra capital provides a necessary cushion for your later years. It’s a pragmatic boost that recognizes the higher costs associated with aging in the current Canadian economy. Take every dollar you’ve earned.

When are the CPP and OAS payment dates for 2025 and 2026?

Government payments hit your bank account on the third to last business day of every month. In 2025, mark your calendar for January 29, February 26, and March 27. Looking ahead to 2026, the first payment is scheduled for January 28. Consistency is the foundation of a professional financial plan. Stop wondering when the money arrives and start directing it toward your lifestyle goals with precision and discipline.

Is the $2,400 OAS increase real for 2025?

No, the rumored C$2,400 flat increase for OAS is a myth circulating online that lacks any basis in federal policy. OAS adjustments happen quarterly based on the Consumer Price Index to ensure your buying power doesn’t erode. While you’ll see incremental boosts in 2025 to match inflation, there’s no massive lump sum coming from the CRA. Get your facts from verified sources and ignore the noise that distracts you from real wealth building.

What is the OAS clawback threshold for the 2025 tax year?

The OAS recovery tax begins if your 2025 individual net world income exceeds C$90,697. If your income climbs above C$148,065 for seniors under 75, the government will claw back your entire OAS benefit. High achievers must be strategic. You’ve worked hard to build a legacy, so don’t let poor tax planning result in a 15 percent penalty on every dollar earned above that threshold. Results require proactive management of your income streams.

Can I receive both CPP and OAS if I am still working in 2026?

You can absolutely collect both CPP and OAS while remaining in the workforce in 2026. If you’re between age 60 and 70, continuing to work while receiving CPP allows you to build the Post-Retirement Benefit. This is a power move for your financial future. It adds a small, permanent increase to your monthly check for the rest of your life. Why stop building momentum just because you’ve reached a traditional retirement age?

How much will the CPP enhancement increase my monthly check in 2025?

The 2025 CPP enhancement introduces a second earnings ceiling of C$81,200, which forces higher contributions but leads to significantly larger payouts. When calculating how much will cpp and oas increase in 2025 canada, remember that these enhancements aim to replace 33 percent of your average work earnings instead of the old 25 percent. This shift represents a breakthrough for long term stability. It’s about scaling your future income through disciplined contributions today.

Will CPP and OAS increases keep up with inflation in 2026?

Both programs are legally mandated to adjust based on the Consumer Price Index, meaning they will track inflation through 2026. OAS adjusts every three months, while CPP sees an annual increase every January. These mechanisms protect your baseline, but they aren’t a strategy for growth. Relying solely on government indexing is a passive approach. You must take ownership of your broader portfolio to ensure your lifestyle outpaces the rising cost of living.