Are you really going to bet your entire financial future on a viral rumor? You’ve likely seen the headlines screaming about oas $2400 payment eligibility, but hope isn’t a strategy. It’s a trap. I know you’re frustrated by the rising cost of living, like the 2.9% inflation rate recorded in January 2024, and the constant noise from conflicting news reports. You want certainty, not clickbait. You deserve a plan that actually works when the bills come due.

In this guide, I’m going to cut through the noise and give you the facts. I’ll expose the truth about these 2026 retirement rumors and, more importantly, show you how to take command of your own monthly cash flow. You shouldn’t have to look to the government for permission to live well. We are going to break down exactly what the Old Age Security program is actually paying and then pivot to a high-performance plan that secures your legacy regardless of what happens in Parliament.

Key Takeaways

- Cut through the noise and verify the hard facts regarding oas $2400 payment eligibility to understand exactly what the 2026 maximums mean for your wallet.

- Master the residency benchmarks and age requirements now so you can stop being a passenger and start dictating your financial terms.

- Protect your prosperity from the 15% “clawback” tax and learn why traditional RRSPs can trigger a massive wealth drain once you hit age 71.

- Shift from government dependency to financial mastery by building a private pension using the Infinite Banking Concept.

- Secure a breakthrough legacy that lasts by moving beyond “average” advice and taking total control of your financial engine.

The $2400 OAS Payment: Separating Fact from Retirement Fiction in 2026

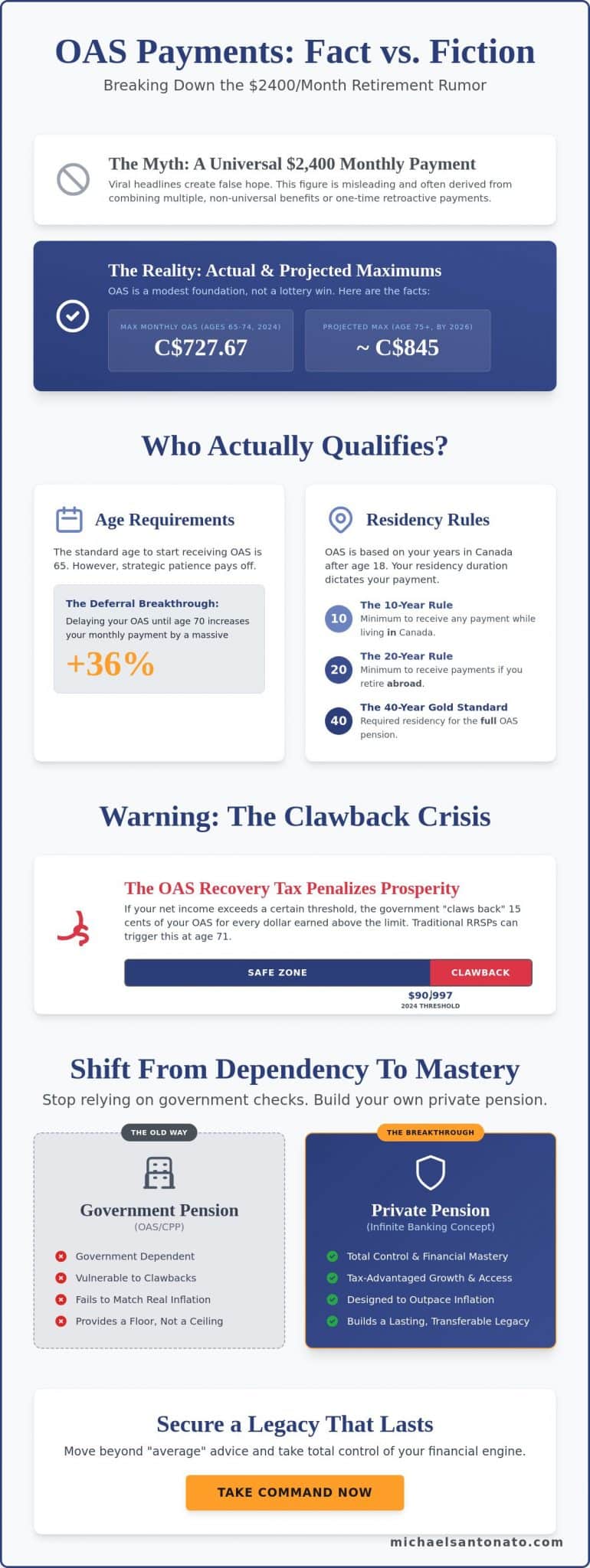

Stop waiting for a miracle check to arrive in your mailbox. The headlines screaming about a $2400 monthly payment are often calculated clickbait designed to exploit your financial anxiety. You need the truth, not a fairy tale. Relying on government “handout hope” is a losing strategy for anyone serious about their legacy. While rumors of a massive windfall circulate on social media, the reality of the Old Age Security (OAS) system is far more pragmatic. If you want to achieve true financial mastery, you must look at the hard data, not the viral noise.

The current maximum monthly OAS payment for 2024 is C$727.67 for those aged 65 to 74. Even with the 10% increase for seniors 75 and older, the check doesn’t come close to $2400. If you are searching for oas $2400 payment eligibility, you must distinguish between a single benefit and a combined household total. Waiting for the government to double your pension is not a plan; it is a retreat from personal responsibility.

Where did the $2400 number come from?

This figure likely stems from a misinterpretation of retroactive payments or the total sum of combined benefits. For some low-income seniors, the combination of OAS, the Guaranteed Income Supplement (GIS), and provincial top-ups might approach this level. However, this is not a universal raise. The rumors surrounding oas $2400 payment eligibility often ignore the strict income thresholds required to trigger maximum GIS supplements. The maximum monthly OAS benefit for seniors aged 75 and over is projected to reach approximately C$845 by 2026, factoring in the permanent 10% increase and standard quarterly cost-of-living adjustments.

- Viral Headlines: Often aggregate three months of payments to create a “shock” number.

- Retroactive Pay: One-time catch-up checks can temporarily inflate a single month’s deposit.

- Combined Benefits: Only those with minimal outside income qualify for the full GIS-OAS stack.

The Reality of 2026 Cost of Living Adjustments

The Consumer Price Index (CPI) dictates your increases, but it is a lagging indicator. When the government announces a 2.5% or 3% increase, it’s often based on data that is already months old. This creates the “Inflation Trap.” Your purchasing power is shrinking in real-time while you wait for a quarterly adjustment that fails to keep pace with 10% spikes in grocery costs or 15% increases in property taxes. You cannot scale your lifestyle on 3% crumbs. To protect your future, you must take control of your own growth at www.truefinancialeducation.com. Real security isn’t found in a CPI adjustment; it’s found in your ability to generate and protect wealth outside of a government system that is designed to provide a floor, not a ceiling.

OAS Eligibility Requirements: Who Actually Qualifies in 2026?

Stop guessing about your future. Retirement isn’t a game of luck; it’s a game of rules. To understand the oas $2400 payment eligibility, you must first master the baseline requirements. The standard entry point is age 65. That’s the threshold. But high performers know that patience pays. If you defer your OAS until age 70, your monthly check increases by 0.6 percent for every month you delay. That is a 36 percent total increase. It’s a massive breakthrough for your cash flow that most people ignore because they’re impatient.

You don’t need a work history to qualify. This isn’t CPP. OAS is about your commitment to this country. It’s about how long you’ve called Canada home. If you want to secure your legacy, you need to know exactly where you stand on the residency scale. The government doesn’t hand these checks out to everyone who asks. You have to prove your presence.

Residency and Legal Status Benchmarks

Living in Canada is the primary requirement, but the duration determines your impact. You need to meet specific benchmarks to unlock your payments:

- The 10-Year Rule: You must have lived in Canada for at least 10 years after age 18 to receive any payment while living in the country.

- The 20-Year Rule: If you plan to retire abroad, you need 20 years of Canadian residency after age 18. If you don’t hit this mark, your payments stop after six months of being away.

- The 40-Year Rule: This is the gold standard. To receive the full OAS pension, you must have lived in Canada for 40 years after turning 18.

If you fall short of 40 years, you receive a partial payment. It’s a simple, cold calculation: (Years in Canada / 40) multiplied by the maximum monthly amount. Don’t let a lack of documentation destroy your oas $2400 payment eligibility when you need it most. You can audit your residency status today to ensure your 2026 reality matches your vision.

Income Thresholds and the “Success Tax”

Success has a price in Canada. It’s called the recovery tax, or the clawback. For 2026, the income threshold is projected to sit around C$95,000, rising from the 2024 baseline of C$90,997. If your net world income exceeds this, the government takes back 15 cents for every dollar over the limit. This is why financial mastery is non-negotiable. You must structure your assets to keep your income below these triggers.

For those at the other end of the spectrum, the Guaranteed Income Supplement (GIS) acts as a critical safety net. It provides extra support if your income is low, but it’s only available if you already qualify for OAS. You can learn more about optimizing your retirement strategy to avoid these traps and maximize your total benefit. High-level performance requires a strategy that protects your wealth from unnecessary erosion. Take action now. Build your plan. Secure your future.

The Clawback Crisis: How the OAS Recovery Tax Penalizes Your Prosperity

You played by the rules. You saved. You invested. You built a life of discipline. Now, the CRA wants to penalize your success. It is called the OAS Recovery Tax, but let’s call it what it really is: a 15% penalty on your hard-earned retirement. If your net world income exceeds the annual threshold, which is C$90,997 for the 2024 tax year, the government starts clawing back your benefits. They take 15 cents for every single dollar you earn above that limit. If you are banking on oas $2400 payment eligibility based on recent 2026 rumors, you must realize that your own savings could disqualify you before the first check even clears.

The irony is staggering. The government encourages you to save for decades, then uses those very savings as a reason to strip away your “guaranteed” benefits. Consider a high-performing professional who retires with a combined income of C$120,000 from various sources. Because they are roughly C$29,000 over the threshold, they face a clawback of over C$4,300. That is thousands of dollars in lost liquidity simply because they were successful. It is a calculated strike against your prosperity.

The RRSP Tax Time Bomb

The RRSP is a trap for the wealthy. It’s sold as a tax-deferred miracle, but for high achievers, it’s a ticking time bomb. At age 71, you’re forced to convert that RRSP into a RRIF. The government then mandates minimum withdrawals every year. These forced payouts count as taxable income. They don’t care if you need the cash; they want their cut. These mandatory withdrawals often push professionals straight into the OAS clawback zone, destroying their oas $2400 payment eligibility and increasing their overall tax bracket. You need to stop following the herd. Learn how to build a fortress around your wealth by reading Infinite Banking Canada: The 2026 Guide to Financial Indestructibility.

Protecting Your Legacy from the Recovery Tax

Stop prioritizing tax-deferred growth. It creates a future liability you cannot control. You must pivot toward tax-free growth and “invisible” income. This is cash flow that doesn’t appear on your T1 return. When you strategically place assets in vehicles like TFSAs or high-cash-value life insurance, that income remains private. It doesn’t trigger the Recovery Tax. You can enjoy a C$150,000 lifestyle while reporting a taxable income of only C$80,000. This isn’t just math; it’s mastery. By mastering asset placement, you stay below the threshold, keep your full OAS payment, and ensure your legacy remains in your hands, not the government’s. Take action now to re-engineer your income before the 2026 changes take effect.

Beyond Government Checks: Building Your Own Private Pension

You’re sitting around waiting for updates on oas $2400 payment eligibility like it’s a rescue boat in a storm. Stop being a passenger in your own life. If your financial security depends on a government rumor or a 2026 policy shift, you’re vulnerable. Real mastery means moving from a state of “eligibility” to a state of “control.” It’s time to build a private pension that doesn’t answer to a politician.

The Financially Indestructible framework is about creating a system that works regardless of what happens in Ottawa. You don’t need a miracle. You need a strategy that prioritizes your own growth over a bureaucrat’s whim. This is how high-performers secure their legacy and ensure they never have to compromise on their lifestyle.

Becoming Your Own Banker

The breakthrough strategy involves the Infinite Banking Concept. You use specialized whole life insurance to create a self-funding retirement. This isn’t your grandfather’s policy; it’s a high-performance cash asset. You use dividends and cash value to fund your lifestyle while your capital continues to compound. Why would you let a bank earn the interest on your money? You should be the one earning it.

- Asset Control: You own the asset 100%. No government department can “adjust” your private wealth.

- Dividend Growth: Your money grows even when you access it for other investments or expenses.

- Cash Flow Redirection: You redirect money you’re already spending into a system you control, building an asset that lasts for generations.

Mastering Cash Flow in Retirement

You need to understand the difference between “income” and “cash flow” in the eyes of the CRA. Traditional income can trigger a massive OAS clawback. For 2024, if your income exceeds C$90,997, the government starts taking your OAS back at a rate of 15 cents for every dollar over the limit. When you access capital through a private banking strategy, you can often do so without triggering a tax event or a clawback.

Are you ready to stop begging for increases and start creating your own? You can’t win a game where the rules change every election cycle. You win by building your own game. Stop worrying about oas $2400 payment eligibility and start focusing on your own private reserve. It’s time to take the wheel.

Ready to stop being a passenger and start driving your financial future? Master your private pension strategy today.

Your Breakthrough Move: How to Secure a Legacy That Lasts

Stop refreshing your browser for news on government handouts. If you spent the last ten minutes searching for oas $2400 payment eligibility, you’re focusing on the wrong side of the ledger. Relying on a government check isn’t a retirement plan; it’s a survival strategy. There’s a massive difference between surviving on what the CRA allows you to keep and thriving through a legacy-driven strategy. One leaves you vulnerable to policy shifts; the other puts you in the driver’s seat.

2026 is your line in the sand. This is the year you stop following “average” financial advice that keeps you tethered to inflation and tax hikes. Average people wait for federal budgets to be passed before they feel secure. Leaders build their own economies. You don’t need more rumors or “leaked” reports. You need a breakthrough that makes you immune to the whims of Ottawa.

The Financially Indestructible Framework

Being Financially Indestructible means your lifestyle doesn’t change when the markets or the politicians do. My framework focuses on three non-negotiable pillars that move you from uncertainty to authority:

- Aggressive Debt Reduction: Stop bleeding interest to the big banks. Reclaim your cash flow to fuel your own growth instead of theirs.

- Tax Optimization: The OAS recovery tax, known as the clawback, kicks in when your net world income exceeds C$90,997 for the 2024 tax year. We structure your assets so you keep your benefits while growing your wealth.

- Wealth Protection: With inflation impacting every Canadian household, you need assets that outpace the cost of living without exposing you to reckless market volatility.

This framework solves the inflation problem before it starts. Don’t wait for the next budget update to know your future. Take command of your cash flow today.

Ready for Mastery?

Government checks are for those who didn’t plan. Mastery is for those who did. If you’re tired of the uncertainty and ready to play at a higher level, it’s time for a different conversation. Private coaching isn’t about getting “tips” on the latest news. It’s about a total shift in how you view money, impact, and legacy.

You have two choices. You can keep chasing rumors about oas $2400 payment eligibility, or you can build a system that makes government payments irrelevant to your success. The path to high-level performance starts with a single decision to stop being a spectator in your own life. Mastery is waiting for you.

Take Command of Your Financial Sovereignty

Waiting for government handouts is a gamble you can’t afford to lose. While rumors about oas $2400 payment eligibility circulate for 2026, the reality is far more complex than a headline. You’ve seen how the OAS recovery tax can strip away your hard-earned prosperity through aggressive clawbacks. Relying on a system that penalizes your success isn’t a strategy; it’s a liability. Since 2012, Michael Santonato has coached Canadian professionals to break free from this cycle using the proven Financially Indestructible framework. As a specialist in Infinite Banking and tax-free wealth planning, Michael helps you build a private pension that the government can’t touch. Don’t let your legacy be defined by a C$2,400 rumor when you can engineer a breakthrough that lasts for generations. It’s time to stop being a spectator in your own financial future and start acting like the leader you are.

Join the Financially Indestructible Program and Stop Relying on Government Checks

Your journey to absolute financial mastery starts with one decisive move. You have the power to build something legendary.

Frequently Asked Questions

Is there really a $2400 OAS payment for seniors in 2026?

No official government source has confirmed a C$2,400 monthly OAS payment for 2026. This figure is a viral myth likely born from a misunderstanding of combined annual benefits or temporary relief programs. Your oas $2400 payment eligibility depends on verified Service Canada updates, not internet speculation. Currently, the maximum monthly payment for seniors aged 75 and over is C$790.16. Don’t build your retirement strategy on rumors; build it on hard data.

Can I receive OAS if I have never worked in Canada?

You can absolutely receive the Old Age Security pension without ever holding a job in Canada. Eligibility is strictly based on your residency history rather than your payroll contributions. You must have lived in Canada for at least 10 years after turning 18 to qualify while residing here. If you live outside the country, that requirement increases to 20 years. Focus on your residency timeline to secure this essential pillar of your retirement income.

What is the maximum income to qualify for OAS in 2026?

Your individual net income must stay below the C$148,065 threshold to receive any OAS if you are under age 75. The recovery tax, or clawback, begins the moment your income exceeds C$90,997 based on 2024 tax year standards. These figures adjust annually to keep pace with inflation. Mastery of your tax brackets is the only way to keep more of your money. Watch these limits closely to ensure your high-performance retirement stays on track.

How much will OAS payments increase in 2026?

OAS payments increase every quarter in January, April, July, and October based on the Consumer Price Index. While the exact 2026 percentage remains unconfirmed, historical data shows a permanent 10 percent increase for seniors aged 75 and over was implemented in July 2022. Expect small, incremental adjustments every three months to match the rising cost of living. Don’t wait for a government windfall. Take action now to grow your own wealth alongside these adjustments.

At what age should I start taking my OAS pension for maximum benefit?

Wait until age 70 if you want the absolute maximum monthly payout from the federal government. Delaying your pension past age 65 increases your payment by 0.6 percent for every month you wait. That adds up to a 36 percent total boost if you hold out for the full five years. Is your current investment portfolio outperforming a guaranteed 7.2 percent annual increase? If not, patience is your greatest financial asset. Take control of your timing today.

What happens to my OAS if I move to another country?

You will continue to receive your OAS payments abroad if you lived in Canada for at least 20 years after your 18th birthday. If you fall short of that 20 year residency mark, the government stops your payments six months after you leave the country. This is a hard rule with no exceptions for personal preference. Plan your international move with these specific residency requirements in mind to avoid a sudden and preventable cash flow crisis.

Does the $2400 figure include the Guaranteed Income Supplement (GIS)?

Rumors regarding oas $2400 payment eligibility often confuse the base OAS pension with the Guaranteed Income Supplement. Even when you combine the maximum GIS with the maximum OAS, a single senior currently receives approximately C$1,760 per month. Reaching a C$2,400 monthly total would require significant provincial top-ups or a massive change in federal policy. Stop chasing phantom numbers. Focus on the maximum guaranteed amounts and bridge the gap with your own investments.

How do I avoid the OAS recovery tax clawback?

Use your TFSA to generate tax-free income that does not count toward the government’s income threshold. Strategic withdrawals from your RRSP before you turn 65 can also help lower your future net income. You should also explore pension sharing with your spouse to keep both individual incomes below the C$90,997 trigger point. High performance requires high-level tax planning. Don’t let the government claw back your hard-earned wealth because you failed to execute a strategy.