Why are you handing over 37% of your top-tier income to the IRS when the rules are designed for you to win? If you feel like a tax slave to the government, it’s because you’re playing a high-stakes game without knowing the scoreboard. You want to know how to pay less tax as a business owner not just to save a few pennies, but to build a legacy that lasts generations. It’s frustrating to watch your hard-earned profit erode under the weight of complex corporate laws while you’re trying to scale your impact.

This is where we draw the line and take control. You can stop the profit hemorrhage and start building a fortress around your wealth today. With the 20% QBI deduction and 100% bonus depreciation now permanent fixtures of the tax code in 2026, the tools for financial mastery are ready for deployment. This article delivers the high-level tax optimization and wealth protection strategies you need to maximize your after-tax income. We’ll explore the exact business structures and private banking concepts required to ensure you remain financially indestructible.

Key Takeaways

- Stop treating tax as a legal obligation and start managing it as your largest business expense to protect your hard-earned legacy.

- Learn exactly how to pay less tax as a business owner by choosing the corporate structure that maximizes your 2026 deferral opportunities.

- Protect your small business tax rate from passive income erosion by understanding the specific thresholds that could grind down your profits.

- Implement the “Waterfall” method to extract wealth strategically, ensuring you utilize capital gains and dividends to get paid first.

- Transition from basic tax preparation to high-level wealth architecture and discover the path to a completely tax-free exit strategy.

Stop Letting Taxes Erode Your Legacy

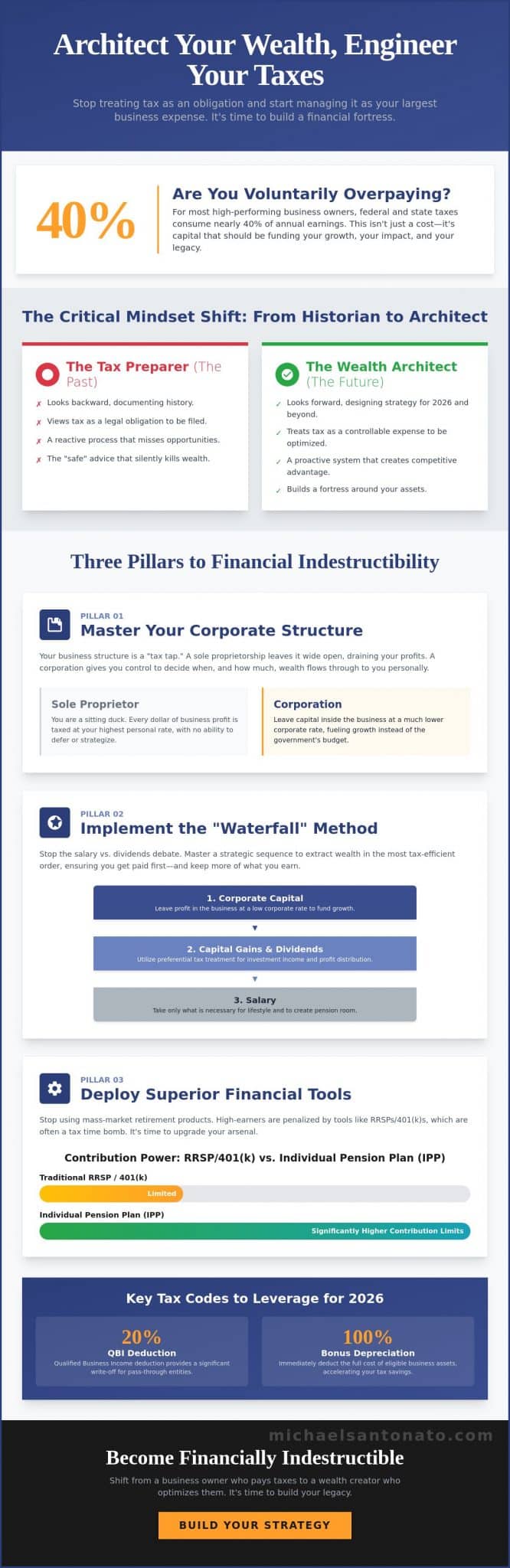

Tax is your single largest line item. Period. You wouldn’t let a landlord overcharge you by 25% on your monthly rent. You wouldn’t tolerate a payroll error that drained your cash reserves by six figures. So why do you accept a tax bill that guts your profit? For most high-performing leaders, federal and state taxes consume nearly 40% of their annual earnings. That is capital that should be funding your next expansion or securing your family’s future. Learning how to pay less tax as a business owner isn’t about cutting corners. It’s about claiming what’s legally yours and treating tax with the same scrutiny as any other operating cost.

The government provides the rulebook. You just need to learn how to play the game. There’s a massive, legal difference between illegal tax evasion and utilizing sophisticated tax avoidance strategies to protect your assets. One gets you a prison cell; the other builds a dynasty. It’s your fiduciary duty to your business and your family to minimize this expense. If you aren’t actively optimizing, you’re essentially giving the government a voluntary tip they didn’t earn.

The High Cost of Average Advice

Most accountants are historians. They look in the rearview mirror to tell you what happened last year. By the time they file your returns, the opportunity to save is dead. This “safe” approach is a silent killer for your wealth. Take the traditional RRSP or 401(k) model. It’s often a tax time bomb for high-earners because you’re deferring tax today only to pay it at the highest marginal rates later when you’re most successful. Tax optimization is a strategic business lever for 2026 that turns a passive obligation into a massive competitive advantage. Stop playing defense with your money.

Defining Financial Indestructibility

Being financially indestructible means your wealth is protected from market volatility and government overreach. Tax efficiency creates the immediate liquidity you need to scale your impact. Without it, you’re running a race with a weight vest on. At Michael Santonato – How To Become Financially Indestructible, we identify the hidden leaks that traditional tax preparers miss every single day. You need a wealth architect who builds for the next decade, not just someone who files for the last quarter. Proactive coaching ensures your business structure is built for how to pay less tax as a business owner while maintaining total compliance. It’s time to shift from a business owner who pays taxes to a wealth creator who optimizes them.

Mastering the Corporate Structure: Beyond Simple Deductions

Most owners think saving on taxes means collecting lunch receipts and tracking mileage. That is small-time thinking. If you want to know how to pay less tax as a business owner, you have to look at your foundation. Are you a sole proprietor? If so, you’re a sitting duck. You’re paying personal tax rates on every single dollar your business earns. By moving into a corporate structure, you gain a “tax tap.” You decide when to turn it on and how much wealth to let through. This allows you to leave capital inside the business at a much lower corporate rate, fueling your next breakthrough instead of the government’s budget.

Competitors often mention the Small Business Deduction (SBD) and its $500,000 limit on active business income. They miss the real strategy. Mastery isn’t just about knowing the limit; it’s about structuring your growth so you don’t hit the “grind down” where passive income erodes your small business status. You can also implement income splitting by paying family members who actually contribute to the business. As long as the pay passes the “reasonableness” test, you’re shifting high-tax income to lower-bracket individuals. It’s a simple, legal move that keeps more money in your family’s hands. If you’re ready to stop guessing, book a strategy session to review your current setup.

Salary vs. Dividends: The Great Debate

In 2026, the extraction method you choose determines your velocity. Salaries are great for creating RRSP or 401(k) room, but they attract heavy payroll taxes. For example, the Social Security wage base has hit $184,500. Once you cross that, you might prefer dividends. Dividends don’t require Social Security or Medicare contributions, keeping your corporation lean. However, you must balance this against your long-term wealth goals. A pure dividend strategy might leave you with zero pension room, which is why a hybrid approach is often the path to financial mastery.

Advanced Write-Offs You Aren’t Using

Stop settling for basic deductions. Individual Pension Plans (IPPs) are superior to RRSPs because they allow for much higher contribution limits funded entirely by your corporation. You should also look at Private Health Services Plans (PHSPs). These allow you to turn personal medical expenses into 100% tax-deductible business costs. Finally, master your timing with Capital Cost Allowance (CCA). With the Section 179 expensing limit at $2.56 million for 2026, timing your asset purchases can wipe out a massive tax bill in a single year. This is how to pay less tax as a business owner at a professional level.

The Passive Income Trap and the Insurance Shield

You’ve worked hard to build a surplus. Now you’re investing it back into the market inside your corporation. Stop. You’re walking straight into a trap that could cost you your small business tax status. In 2026, the government isn’t just taxing your investment gains; they’re using those gains to “grind down” your access to lower tax rates on your active business income. This is the hidden tax that destroys momentum. If you want to know how to pay less tax as a business owner, you must protect your active income from being reclassified and overtaxed due to your passive success.

Here is the math you need to master. For every $1 of passive income your corporation earns over the $50,000 threshold, your small business deduction limit is reduced by $5. Once you hit $150,000 in passive income, that lower rate is completely gone. You’re suddenly paying the high general corporate rate on every dollar of active profit. This isn’t just a minor fee; it’s a structural failure that hemorrhages profit. You need a strategy that keeps your passive growth from triggering this threshold while still allowing your wealth to compound.

Why Traditional Corporate Investing is Broken

Investing surplus cash in traditional taxable accounts inside your company is a losing game. Corporate passive income is often taxed at rates exceeding 50%. You’re effectively working for the government half the time. To achieve financial mastery, you must move money from “taxable” buckets into “tax-exempt” buckets legally. Understanding Infinite Banking Canada: The 2026 Guide to Financial Indestructibility is the first step toward reclaiming your profit and securing your breakthrough.

The Infinite Banking Advantage

High-performance owners use permanent life insurance as a “tax-free vault.” This isn’t about a death benefit; it’s about control. By holding corporate surplus in a properly structured policy, you shield that capital from the passive income grind. You can then use the Infinite Banking Concept to finance business equipment or growth by borrowing against your own cash value. This creates a self-funding business model that generates tax-free legacy wealth. Infinite Banking turns a tax liability into a cash flow asset that works for you 24/7. This is how to pay less tax as a business owner while maintaining the liquidity needed for rapid scaling.

Strategic Wealth Extraction: How to Get Paid First

You are the engine of your business. You take the risks. You put in the hours. You deserve to get paid first. Most owners wait for the scraps left over after the government takes its cut. That is a loser’s game. To achieve true financial mastery, you need to implement the “Waterfall” method of wealth extraction. This isn’t just about a paycheck. It’s about a systematic flow of capital that starts with tax-deductible expenses, moves into dividends, and eventually culminates in capital gains. This is the blueprint for how to pay less tax as a business owner while building a fortress of personal wealth.

One tool many owners misuse is the shareholder loan. It’s a powerful way to access short-term liquidity without immediate tax consequences. However, you must avoid the “two-year” trap. If you don’t repay that loan within one year of the corporation’s tax year-end, the CRA will treat that entire amount as personal income. That mistake can trigger a massive tax bill and an audit you didn’t ask for. Discipline is the price of freedom. Use the rules, but don’t let them use you.

The Holding Company Power Play

A holding company (Holdco) is your second layer of defense. It acts as a private vault for your surplus. By using inter-corporate dividends, you can move retained earnings from your operating company to your Holdco tax-free. This protects your hard-earned cash from potential creditors and lawsuits. It also provides the perfect environment for Michael Santonato – How To Become Financially Indestructible strategies. Instead of leaving cash sitting idle in a bank account where it’s vulnerable, you move it into a structure that grows and protects your legacy simultaneously.

Preparing for the Ultimate Payday

Your business is an asset, not just a job. You should structure it for sale from day one. In 2026, the Lifetime Capital Gains Exemption (LCGE) remains one of the greatest tax gifts available to entrepreneurs. It allows you to walk away with a massive chunk of your sale price completely tax-free. But there’s a catch. Your corporation must be “purified.” This means at least 90% of your assets must be used in active business at the time of sale. If you’ve let too much passive cash sit in the operating company, you lose the exemption. Is this legal? Yes. It’s about proactive planning, not tax evasion. If you want to ensure your exit is as profitable as possible, book your strategic extraction audit today.

Build Your Financially Indestructible Business

Stop settling for historians when you need an architect. Most business owners rely on a tax preparer to tell them how much they owe after the damage is already done. That is a reactive, losing strategy. If you want to master how to pay less tax as a business owner, you need a Wealth Architect who designs your future. You need a framework that anticipates changes in the 2026 tax landscape and builds a perimeter around your profit. This is about moving from the confusion of complex codes to the absolute clarity of a proven system.

The Financially Indestructible Coaching Program is that system. It’s not a generic checklist; it’s a high-octane roadmap to total financial independence. We don’t just look at your filings. We audit your entire corporate architecture to identify the leaks that are draining your momentum. Taking “The Wake Up Call” means acknowledging that your current path might be costing you six figures in unnecessary payments. Audit your structure before this tax year ends. The government won’t send you a thank-you note for overpaying, but your family will certainly feel the impact of the wealth you choose to keep.

Master Your Craft, Scale Your Purpose

Tax optimization is the bedrock of a lasting legacy. When you reclaim your capital, you gain the fuel to scale your purpose and impact the world on your terms. This isn’t just about spreadsheets; it’s about integrating your personal values into your corporate strategy. You work too hard to let inefficient structures dictate your ceiling. To dive deeper into this framework and start your breakthrough, I encourage you to Get the Book. It’s time to stop being a spectator in your own financial life and start mastering your craft.

The Time to Act is Now

Delay is the most expensive tax you’ll ever pay. Every month you wait to optimize is another month of hemorrhaging profit that you can never recover. If you’re earning over $200,000 and still following “safe” advice, you’re likely losing thousands of dollars every thirty days. Join the elite group of high-performers who have decided to stop being tax slaves and start being wealth creators. The rules for 2026 are set. The strategy is clear. Your legacy is waiting. Book your strategy session for the Financially Indestructible Program today and take command of how to pay less tax as a business owner.

Claim Your Financial Mastery Today

You’ve seen the map. You know the scoreboard. Every day you operate without a strategic architecture, you’re choosing to fund the government’s legacy instead of your own. We’ve covered the power of corporate structures, the danger of the passive income trap, and the necessity of getting paid first through the waterfall method. This is not just theory. As the founder of the Financially Indestructible framework and a specialist in Infinite Banking for high-net-worth owners, I’ve spent decades distilling real-world wealth protection into actionable results.

Mastering how to pay less tax as a business owner is the ultimate lever for your growth. You have the right to keep what you earn and the duty to protect it for those who follow you. Don’t let another tax year slip away while you’re stuck in a reactive cycle. It’s time to shift from a tax slave to a wealth creator. Your breakthrough is one decision away. Stop hemorrhaging profit and start building a fortress around your family’s future.

Master your wealth and pay less tax; Join the Financially Indestructible Program today!

Frequently Asked Questions

Is it better to pay myself a salary or dividends as a business owner in 2026?

You should choose dividends to avoid the 15.3% self-employment tax or the Social Security tax on earnings up to the $184,500 wage base. Dividends keep your corporation lean because they don’t require payroll tax contributions. However, if you want to create retirement deferral room in an RRSP or 401(k), a salary is a requirement. Most high-performers use a hybrid approach to balance immediate cash flow with long-term wealth extraction.

How can I legally reduce my corporate tax rate in Canada or the US?

You reduce your rate by moving from a sole proprietorship to a corporate structure where the federal rate is a flat 21% in the US or significantly lower for small businesses in Canada. This is the foundation of how to pay less tax as a business owner. By stopping the flow of income to your personal return, you avoid marginal rates as high as 37% and keep more capital for growth.

What is the Small Business Deduction and how do I keep it?

The Small Business Deduction is a tax credit that lowers your corporate tax rate on the first $500,000 of active business income. To keep this advantage, you must ensure your passive investment income stays below the $50,000 threshold. If your passive earnings climb too high, the government “grinds down” your deduction, forcing you to pay the much higher general corporate tax rate on every dollar of profit.

Can I use a life insurance policy to pay less business tax?

You can use a properly structured whole life policy to create a tax-exempt vault for your corporate surplus. This strategy utilizes the Infinite Banking Concept to shield your money from the passive income grind that destroys small business tax rates. It turns a traditional insurance cost into a living cash flow asset that grows sheltered from taxes while providing liquidity for your next business breakthrough.

What business expenses are the most commonly missed by owners?

Most owners miss Private Health Services Plans and the Section 179 expensing limit, which allows you to deduct up to $2.56 million in equipment purchases for 2026. You should also maximize HSA contributions, which are $4,400 for individuals and $8,750 for families this year. These aren’t just minor write-offs; they are structural tools that transform personal medical and equipment costs into 100% tax-deductible corporate expenses.

How does a holding company help with tax optimization?

A holding company acts as a legal firewall that allows you to move retained earnings out of your operating company tax-free through inter-corporate dividends. This protects your hard-earned surplus from potential lawsuits or creditors while maintaining your investment flexibility. It’s a critical layer in your corporate architecture that ensures your wealth stays in your control rather than being exposed to unnecessary risks or taxes.

What is the “Passive Income Trap” for corporations?

The trap is a rule where every $1 of passive investment income over $50,000 reduces your small business limit by $5. If your corporation earns $150,000 in passive income, your access to the lower small business tax rate vanishes completely. You must use tax-exempt vehicles like Individual Pension Plans or life insurance to ensure your investment success doesn’t trigger a massive tax hike on your active business earnings.

How do I know if my current accountant is doing enough for my tax planning?

Your accountant is failing you if they only talk about the past during tax season instead of projecting your future growth. A true wealth architect meets with you quarterly to implement proactive strategies for how to pay less tax as a business owner before the year ends. If they aren’t suggesting structural changes or wealth extraction methods like the waterfall approach, they are just a compliance officer, not a partner.